The Best Credit Cards for High-Net-Worth Individuals

Written by: Tess Nakaishi

Updated June 2026

2026 High-Net-Worth Asset Allocation Report

See how high-net-worth investors with an average net worth of $17M are allocating across public equities, private markets, real estate, bonds, and cash. Based on benchmark data from 230+ respondents.

Most credit card comparisons start with the wrong question. They ask which card earns the most. Long Angle members ask a different one: which card fits my life without requiring me to think about it every month?

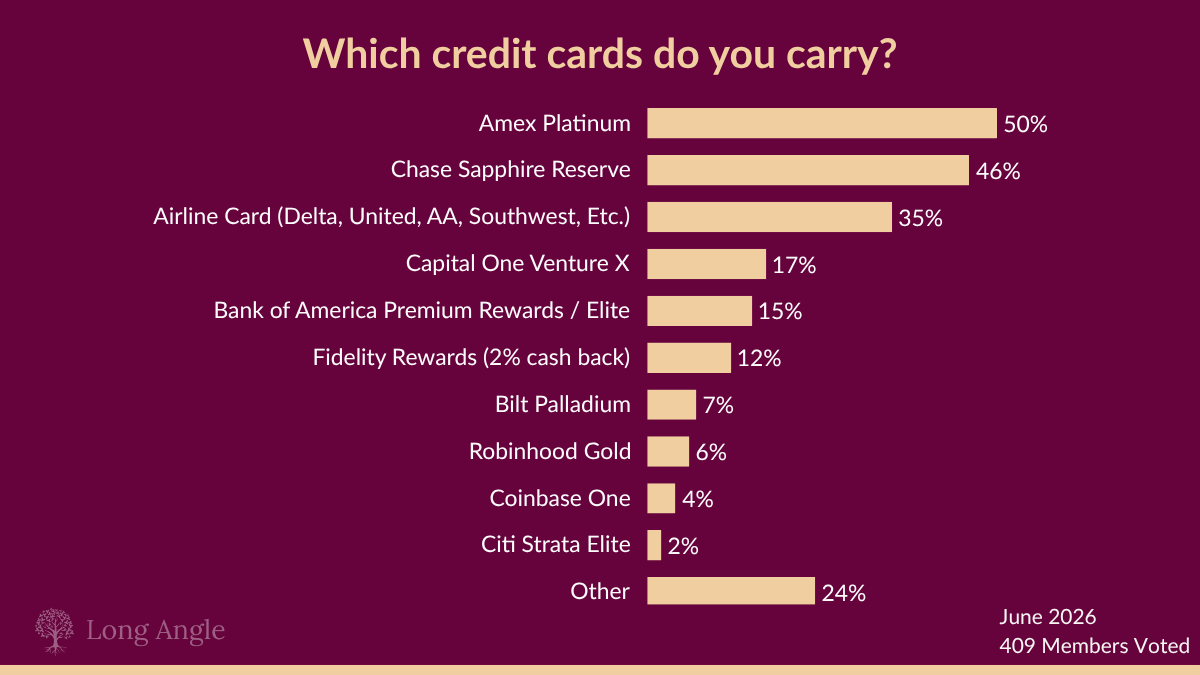

Long Angle has polled members on credit card usage twice, in 2024 and again in June 2026. The results shifted in ways worth understanding. In 2026, American Express Platinum edged ahead as the most common primary card (25%), with Chase Sapphire Reserve close behind at 24%. When asked which cards they carry, Amex Platinum leads at 50% and Chase Sapphire Reserve sits at 46%. The two are nearly interchangeable in terms of how broadly they're held, but how members use them has diverged in ways the data alone doesn't capture.

This post covers the five cards members use most, what changed with each since 2024, and the framework members use to decide.

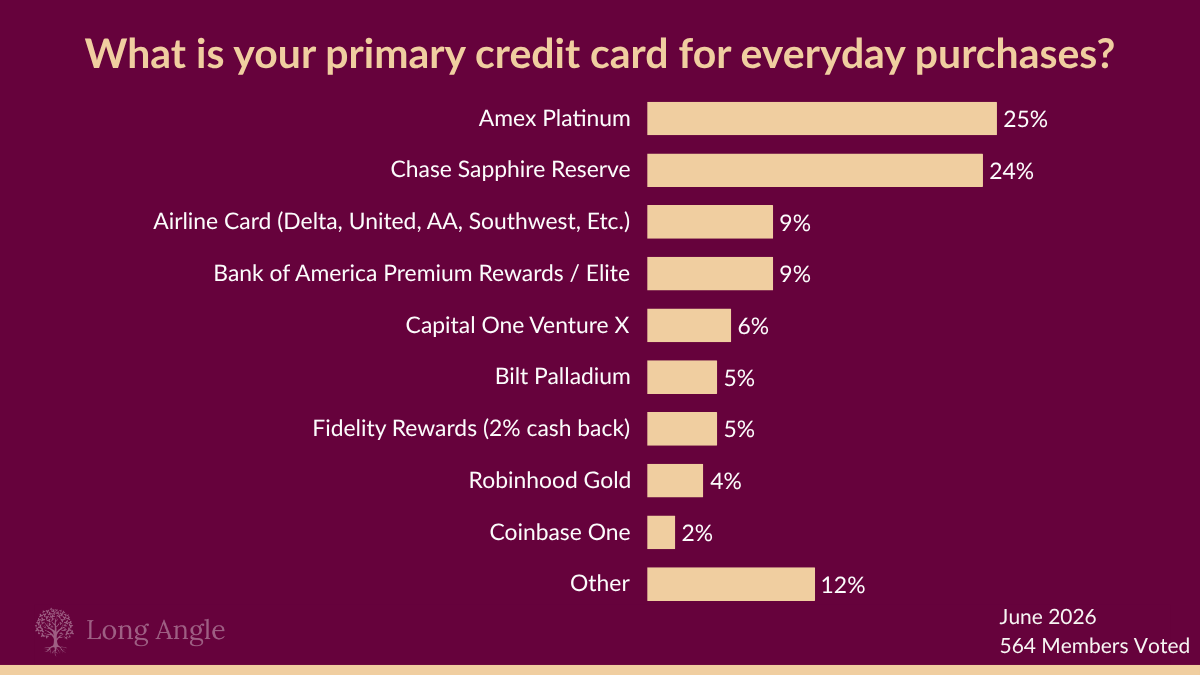

The most commonly carried credit cards among Long Angle members, based on a June 2026 poll of 409 members, are American Express Platinum (50%), Chase Sapphire Reserve (46%), airline cards (35%), Capital One Venture X (17%), and Bank of America (15%). As a primary daily card, Amex Platinum leads at 25% and Chase Sapphire Reserve follows at 24%. Card selection at this wealth level is less about maximizing every basis point and more about finding a setup that fits spending patterns, travel habits, and tolerance for complexity.

Key Takeaways

In a June 2026 Long Angle poll of 564 members, American Express Platinum edged ahead of Chase Sapphire Reserve as the most common primary card (25% vs. 24%), a reversal from 2024 when Chase dominated

Members overwhelmingly use two premium cards rather than one: Amex Platinum and Chase Sapphire Reserve are each carried by roughly half of respondents, most often in combination

Airline cards rose significantly, now carried by 35% of members, suggesting members are using premium cards for earning and airline cards as functional complements for lounge access and companion fares

Bilt Palladium and Robinhood Gold entered the poll for the first time and combined for 9% of primary card usage, reflecting genuine movement in member behavior since 2024

Card terms have changed materially: the Amex Platinum fee rose to $895, the Chase Sapphire Reserve fee rose to $795, and the BofA Preferred Rewards Platinum Honors tier now requires $1M in qualifying assets (up from $100K)

Table of Contents

How High-Net-Worth Members Think About Credit Cards

Credit card threads in Long Angle generate strong opinions, but not always about what you'd expect. The most recurring theme is not which card earns the most. It is whether optimizing cards is worth the time at all.

One member laid out a priority stack that has come up repeatedly in community discussions: investments first, tax strategies second, credit card points well down the list. Another noted that many members spend more mental energy on credit card optimization than on investment strategy and questioned whether the math ever justifies that. These are not fringe views. They reflect how a meaningful portion of high-net-worth members approach this topic.

That said, the members who do optimize are often operating at a different scale than a typical consumer. Members running $500K or more per year in advertising spend through business cards, members with multiple rental property mortgages, and members who fly international business class several times a year can generate tens of thousands of dollars in annual value from a well-constructed card setup. One member described booking a six-person safari with international business class tickets using points accumulated through high business card spend. For these members, the math genuinely works.

What emerges across Long Angle discussions is three recognizable approaches:

Maximum simplicity. One primary card for almost everything. This setup works best when travel is light, schedules are full, and managing a points system feels like a project nobody has time for. Several members in this group direct their cash back straight into investment accounts, treating the card as a passive savings mechanism rather than a perks vehicle.

Value without complexity. A two-card setup, one for travel and dining, one for everything else. This is the most common configuration among Long Angle members who want most of the upside with minimal ongoing attention. A premium travel card paired with a flat cash back card is the setup that appears most often in member discussions.

Optimization. A full points ecosystem built around sign-up bonuses, transfer partners, and award redemptions. This approach works best for members who enjoy the process and have the travel volume to use what they accumulate. Several Long Angle members have described booking business class to Europe or Japan for the equivalent of $600 to $800 in points, a result that is difficult to match with any cash back card.

A recurring pattern: members often start in the optimization camp, then migrate toward simplicity as their time becomes more constrained. The destination is usually the two-card setup.

None of this is a recommendation. The five cards below are the ones members use most. Which setup is right depends on how a member answers one question honestly: how much time am I willing to spend on this?

What the 2026 Poll Tells Us

The June 2026 Long Angle poll is meaningfully different from the 2024 version in both scale and structure. In 2024, 308 members answered a single "select all that apply" question, and Chase Sapphire Reserve dominated at 54%. In 2026, 564 members answered two questions: which card is your primary, and which do you carry. That distinction matters.

Source: Long Angle Community Poll, June 2026

On the primary card question, Amex Platinum (25%) and Chase Sapphire Reserve (24%) are essentially tied. The more revealing finding is what changed: Bilt Palladium entered at 5% and Robinhood Gold at 4%, two cards that did not exist in the 2024 poll options. Together they account for 9% of primary card usage, which reflects genuine behavioral movement among members since 2024.

Source: Long Angle Community Poll, June 2026

On the "cards carried" question, Amex Platinum and Chase Sapphire Reserve are carried by roughly half of respondents each, which means most members who have one also have the other. The question is which they treat as primary. The thread discussion makes the split clear: members typically use Amex Platinum for flights (5x direct with airlines), Centurion Lounge access, and lifestyle credits, and Chase Sapphire Reserve for hotel and dining spend, or vice versa depending on their spending profile.

Airline cards rose to 35% carried, up from 12% in the 2024 poll. Several members in the thread explained the logic: premium cards for earning, airline cards as functional complements for companion fares, lounge access at specific hubs, and co-branded benefits that premium cards cannot replicate.

The 24% "Other" on the carried question reflects the long tail of cards members run for specific purposes: Amazon Prime Visa for Amazon and Whole Foods spend, Alaska Airlines cards for companion fares, co-branded hotel cards for status, and newer entrants like the Citi Double Cash and Fidelity Rewards Visa for members who want simple flat cash back without any annual fee.

Credit Card Features to Evaluate

Different features matter more depending on individual lifestyle and spending patterns. A few elements to consider when evaluating cards at this wealth level:

Cash Back vs. Points

Many high-net-worth individuals prefer cash back for its simplicity and universal value. A flat-rate cash back card requires no category tracking, no portal bookings, and no point valuations.

Points and miles are advantageous for members who travel frequently, particularly internationally, where business and first class redemptions can generate 5 to 10 cents per point in effective value. Cards like the Chase Sapphire Reserve and Amex Platinum are built around travel rewards and offer strong multipliers on flights and hotels.

There is no universally right answer. A 2024 survey found that 59% of Americans with net worths over $1 million own cash back credit cards, while 49% have travel rewards cards. Among Americans with net worths under $1 million, 72% have cash back cards versus 23% with travel cards. High-net-worth individuals skew toward travel rewards relative to the broader population, but a significant share still prefer simplicity.

Convenience

At higher spending levels, the ability to request a higher credit limit by phone, access to a dedicated customer service team, and reliable concierge service matter more than they do for average cardholders. Several premium cards now offer lounge access as a practical benefit for members who travel frequently.

Fees

Annual fees on premium cards range from $0 to $895. The higher the fee, the more actively a member needs to use the associated credits to justify it. The Amex Platinum at $895 per year requires consistent engagement with its credit ecosystem: Resy dining credits, Uber Cash, hotel benefits, lounge access, and more. Members who travel frequently and use those credits regularly can extract well over the annual fee in value. Members who travel occasionally may not.

One pattern that emerged in the 2026 thread: several members described getting the Amex Platinum through Morgan Stanley and having the annual fee effectively covered through the Morgan Stanley Annual Engagement Bonus, which requires maintaining a qualifying relationship with Morgan Stanley. For members already banking or investing there, this arrangement makes the card essentially free.

Other Perks

Premium cards typically include welcome bonuses, travel protections, airport lounge access, hotel status, and a range of statement credits. The most important question is not how large the list of perks is, but how many of them a member will use consistently.

Beyond Wealth Newsletter

Weekly perspectives on money, decisions, and the financial questions that matter at this stage. Read by founders, executives, and investors navigating the same topics covered in this post.

The 5 Best Credit Cards for High-Net-Worth Individuals

Long Angle polled members in 2024 and again in June 2026. The five cards below represent the most widely held options in both polls, with current terms as of June 2026. Card terms change frequently; verify current details before applying.

Chase Sapphire Reserve

The Basics

Annual Fee: $795

APR: 19.49%–27.99% variable

Welcome Offer: 125,000 points after spending $6,000 in the first 3 months

Earning Rates

8x points on all Chase Travel purchases (flights, hotels, rental cars, cruises, activities)

4x points on flights booked directly with airlines

4x points on hotels booked directly

3x points on dining worldwide

1x points on all other purchases

Key Benefits

$300 annual travel credit (applies to any travel purchase, the most flexible credit available on any premium card)

$500 annual credit for stays with The Edit (Chase's handpicked hotel collection), up to $250 per booking with a two-night minimum

$300 annual dining credit via Sapphire Exclusive Tables on OpenTable

$300 annual StubHub and viagogo credit (through 12/31/2027)

Access to Chase Sapphire Lounges by The Club plus 1,300+ Priority Pass lounges worldwide with up to two guests

Complimentary Apple TV and Apple Music subscriptions ($288 value, through 6/22/2027)

IHG One Rewards Platinum Elite status (through 12/31/2027)

Global Entry, TSA PreCheck, or NEXUS fee credit (up to $120 every four years)

Points Boost: points worth up to 2x on select hotels and flights through Chase Travel

Reserve Travel Designers: personalized trip planning service (value up to $300 per trip)

No foreign transaction fees

1:1 point transfer to leading airline and hotel loyalty programs

Comprehensive travel protections: trip cancellation/interruption up to $10,000 per traveler, primary auto rental coverage up to $75,000, emergency evacuation up to $100,000

Cons: Highest reward rates require booking through the Chase Travel portal; the $795 annual fee requires consistent use of credits to justify; portal bookings are agency tickets, which can create friction in disruption scenarios

Best for: Frequent travelers who want one premium card and are willing to book travel through Chase's portal to maximize returns; members who pair it with Amex Platinum typically use it for hotels, dining, and portal-based bookings

American Express Platinum

The Basics

Annual Fee: $895

APR: 19.49%–28.49% variable (Pay Over Time feature)

Welcome Offer: up to 175,000 Membership Rewards points after spending $12,000 in the first 6 months (welcome offers vary and you may not be eligible)

Earning Rates

5x points on flights booked directly with airlines or through American Express Travel (up to $500,000 per calendar year)

5x points on prepaid hotels booked through American Express Travel

1x points on all other purchases

Key Benefits

$600 annual hotel credit ($300 semi-annually) for Fine Hotels + Resorts or The Hotel Collection bookings through Amex Travel

$400 annual Resy dining credit ($100 per quarter) at U.S. Resy restaurants

$300 annual digital entertainment credit ($25/month)

$300 annual Equinox credit (Equinox+ subscription or club membership)

$209 annual CLEAR+ credit

$200 annual Uber Cash ($15/month plus $20 in December)

$200 annual airline fee credit (select one airline)

$200 annual Oura Ring credit

$155 annual Walmart+ credit

$300 annual lululemon credit ($75/quarter)

Access to 1,550+ airport lounges through the Global Lounge Collection, including Centurion Lounges, 10 Delta Sky Club visits per year, and Priority Pass Select membership

Complimentary Hilton Honors Gold status and Marriott Bonvoy Gold Elite status

Global Entry ($120) or TSA PreCheck (up to $85) credit every four years

Fine Hotels + Resorts: guaranteed 4pm checkout, daily breakfast for two, average total value over $550 per stay

Concierge service

No foreign transaction fees

1:1 point transfers to 20+ airline and hotel partners

Note: The Saks Fifth Avenue credit is being discontinued effective July 1, 2026. Morgan Stanley clients with a qualifying CashPlus Platinum account may be eligible to have the annual fee covered through the Morgan Stanley Annual Engagement Bonus program; confirm eligibility with Morgan Stanley directly.

Cons: At $895, the annual fee requires active engagement with a wide range of credits to justify; most credits require separate enrollment or manual activation; earning 5x on hotels requires booking through Amex Travel rather than direct

Best for: Members who travel frequently and will consistently engage with the credit ecosystem; also well-suited as a complementary card to Chase Sapphire Reserve, with members using it primarily for direct airline bookings (5x), Centurion Lounge access, and lifestyle credits

Prime Visa

The Basics

Annual Fee: $0

APR: 18.74%–27.49% variable

Welcome Offer: $150 Amazon Gift Card on approval (requires eligible Prime membership)

Earning Rates

6% back on eligible Amazon.com purchases when selecting certain delivery methods

5% back at Amazon.com, Amazon Fresh, Whole Foods Market, and on Chase Travel purchases (requires eligible Prime membership)

2% back at gas stations, restaurants, and on local transit and commuting (including rideshare)

1% back on all other purchases

Key Benefits

Daily rewards: points credited as soon as the next day, redeemable at Amazon checkout or through Chase for cash back, gift cards, or travel

No annual credit card fee

No foreign transaction fees

Travel and purchase protections including lost luggage reimbursement, baggage delay insurance, travel accident insurance, and purchase protection

10% back or more on rotating Prime Card Bonus items and categories (limited-time offers)

Cons: Requires an active Amazon Prime membership ($139/year); highest rewards rates are Amazon-specific

Best for: Members who shop frequently at Amazon, Amazon Fresh, or Whole Foods and want a no-fee card that earns meaningfully on those purchases; frequently used as a third card alongside two premium cards rather than a primary

Capital One Venture X

The Basics

Annual Fee: $395

APR: 19.49%–28.49% variable

Welcome Offer: 75,000 miles after spending $4,000 in the first 3 months

Earning Rates

10x miles on hotels and rental cars booked through Capital One Travel

5x miles on flights and vacation rentals booked through Capital One Travel

5x miles on Capital One Entertainment purchases

2x miles on all other purchases

Key Benefits

$300 annual travel credit for bookings through Capital One Travel

10,000 anniversary bonus miles every year starting on the first anniversary (equal to $100 toward travel)

Global Entry or TSA PreCheck credit up to $120

Access to Capital One Lounges and 1,300+ Priority Pass lounges worldwide

Premier Collection: $100 experience credit, daily breakfast for two, room upgrades, early check-in and late checkout at luxury hotels and resorts

Lifestyle Collection: $50 experience credit and premium benefits per stay

Complimentary PRIOR subscription (destination guides, exclusive trip access)

Hertz Gold+ status upgrade

50% off a Cultivist Enthusiast membership for up to two years (note: previously listed as a complimentary membership; the benefit has changed)

Complimentary 6-month Vinous wine subscription

Cell phone protection up to $800

No foreign transaction fees

Miles transferable to 15+ travel loyalty programs; no expiration

Cons: Highest earning rates require booking through the Capital One Travel portal; the Cultivist benefit has been reduced from complimentary membership to a discount; the Capital One and Citi points ecosystems are generally considered less flexible than Chase Ultimate Rewards or Amex Membership Rewards

Best for: Frequent travelers looking for a lower annual fee premium travel card with strong everyday earning and flexible mile redemption; often used as an everyday spend card by members who want 2x on everything without restricting themselves to a specific points ecosystem

Bank of America Unlimited Cash Rewards

The Basics

Annual Fee: $0

APR: 17.49%–27.49% variable

Welcome Offer: $200 cash rewards bonus after spending $1,000 in the first 90 days

Earning Rates

2% cash back on all purchases for the first year from account opening

1.5% cash back on all purchases thereafter

BofA Rewards members earn a bonus on top of the base rate based on qualifying tier (see below)

Key Benefits

No cap on cash back earnings; rewards do not expire as long as the account is open

0% intro APR for first 15 billing cycles on purchases and balance transfers made within the first 60 days

Flexible redemption: statement credit, deposit to Bank of America or Merrill account, or check

BofA Rewards program: members with qualifying assets at Bank of America or Merrill earn a bonus on cash back

| Tier | Qualifying Assets | Bonus | Effective Rate (after year 1) |

|---|---|---|---|

| Gold | $20K–$50K | 25% | 1.87% |

| Platinum | $50K–$100K | 50% | 2.25% |

| Platinum Honors | $1M+ | 75% | 2.625% |

Important note: As of May 2026, the Platinum Honors tier now requires $1M or more in qualifying Bank of America deposit and Merrill investment accounts, increased from the prior $100K threshold. Members who previously qualified for the 75% bonus at $100K will see their bonus rate reduced unless they meet the new $1M requirement. The change takes effect based on your program anniversary date, with a six-month transition period beginning May 26, 2026. Despite this change, some Long Angle members continue to use this card for tax payments and other large transactions where its straightforward cash back and high cycling tolerance make it practical.

Cons: Base rate reverts to 1.5% after the first year; the highest cash back rate now requires $1M in qualifying assets at Merrill; verify whether a foreign transaction fee applies before international use

Best for: Members who want a simple flat cash back card and either have $1M in qualifying Merrill assets or are comfortable with the 1.5%–1.87% base rates; particularly useful for large one-time payments like estimated taxes and property taxes

Comparison Table

| Chase Sapphire Reserve | Amex Platinum | Prime Visa | Capital One Venture X | Bank of America | |

|---|---|---|---|---|---|

| Annual Fee | $795 | $895 | $0 | $395 | $0 |

| Welcome Offer | 125,000 points after $6,000 in 3 months | Up to 175,000 points after $12,000 in 6 months | $150 Amazon Gift Card on approval | 75,000 miles after $4,000 in 3 months | $200 bonus after $1,000 in 90 days |

| Top Earning Rate | 8x on Chase Travel | 5x on direct airline bookings and prepaid hotels through Amex Travel | 6% on select Amazon delivery; 5% at Amazon/Whole Foods/Chase Travel | 10x on hotels and rental cars through Capital One Travel | 2% first year, 1.5% thereafter (up to 2.625% with BofA Rewards Platinum Honors) |

| Reward Form | Points | Points | Cash back | Miles | Cash back |

| Key Catch | Highest rates require Chase Travel portal bookings | $895 fee requires active credit utilization; most credits need separate enrollment | Requires Prime membership ($139/year) | Cultivist benefit reduced from complimentary to discounted; best rates require Capital One Travel portal | Platinum Honors rate (2.625%) now requires $1M in Merrill/BofA assets |

| 2026 Poll (Primary) | 24% | 25% | Not polled separately | 6% | 9% (BofA Premium Rewards / Elite) |

| 2026 Poll (Carried) | 46% | 50% | Not polled separately | 17% | 15% |

| Best For | Frequent travelers wanting one premium card; pairs well with Amex Platinum | Members who actively use lifestyle and travel credits; pairs well with Chase Sapphire Reserve | Frequent Amazon and Whole Foods shoppers | Travelers wanting lower fee with strong everyday earning | Large one-time payments and members preferring flat cash back |

Credit Card Diversification

The 2026 poll makes the most common two-card setup explicit: Amex Platinum and Chase Sapphire Reserve are each carried by roughly half of members, and the thread confirms most members who have one also have the other. The logic is straightforward. Amex Platinum leads on direct airline spend (5x), Centurion Lounge access, and lifestyle credits. Chase Sapphire Reserve leads on hotels booked direct (4x), dining (3x), and flexibility through Chase Travel. Together they cover most high-spend categories without requiring a third card for most members.

For members who want simplicity above all, either card used alone provides strong coverage. The annual fees are meaningful, but members who travel regularly and engage with the associated credits typically come out ahead on both.

For members drawn to optimization, the most frequently discussed approach is building around a strong points currency (Chase Ultimate Rewards or Amex Membership Rewards) and using transfer partners to book business class flights at a fraction of the cash price. Members who have done this describe it as one of the highest-return uses of time in their financial lives, but only if travel volume and schedule flexibility support it.

Multi-card portfolios beyond two add complexity. Managing category bonuses, credit limits, and annual fee renewal decisions across five or more cards is a project. Before building a complex stack, the honest question is whether the incremental return justifies the ongoing overhead.

Where do high-net-worth members compare notes on credit card strategy, cashflow optimization, and how their card setup fits their broader financial picture?

Long Angle is a vetted community where members share what they've found works at $5M+ net worth, without anyone in the room selling a card or earning a commission. The environment is solicitation-free and the recommendations come from direct experience.

How to Optimize Credit Card Use

For members who want to extract more value from their card setup, a few approaches that come up consistently in Long Angle discussions:

Welcome bonuses are the highest-return moment in any card relationship. A well-timed application tied to a large known expense (home renovation, tax payment, tuition) can generate $1,500 to $3,000 in points value from a single spend threshold. Members who have churned through Chase Ink business cards for their sign-up bonuses and then transferred points to Chase Sapphire Reserve for redemption have described accumulating hundreds of thousands of points without significantly increasing their ongoing spend.

When redeeming points for flights, going directly through the airline rather than through a card portal typically produces better value and cleaner service when something goes wrong. Portal bookings are agency tickets. Airlines treat them differently in disruption scenarios, and some carriers will not rebook or reroute portal passengers without routing through the agency first.

Points valuations change. Resources like The Points Guy publish monthly point valuations that reflect current transfer partner redemption rates. The difference between a 1-cent and a 2-cent redemption on the same points balance is the difference between getting $1,000 and $2,000 in value.

Paying estimated taxes with a credit card generates meaningful cash back or points on large payments. Members running the BofA card at 2.625% on a $100,000 quarterly tax payment earn $2,625 on a transaction they would make regardless. Note that Bilt Palladium does not earn rewards on tax payments, a limitation that has come up repeatedly in community discussions.

For members managing multiple cards, tools like Empower, Monarch Money, or Kubera can sync transactions across cards into a single view, reducing the administrative overhead of a multi-card setup.

Transfer bonuses are time-limited and recurring. Several Long Angle members have described doubling their effective point value by timing transfers to airline partners during promotion windows. One member described doubling a JAL transfer during a bonus promotion to book a Japan trip. These windows are worth monitoring for members with large point balances.

Seats.aero and similar tools help members find award availability across multiple programs before committing to a redemption. Members who find that a specific route is never available on their primary program often discover it is available through a transfer partner.

Cards Members Are Also Watching

The five cards above cover what most Long Angle members use for everyday personal spending. The 2026 poll and thread discussion surfaced meaningful movement toward a second tier of cards that did not appear in the 2024 poll.

Bilt Palladium entered at 5% primary and 7% carried. Members with large mortgage portfolios, including rental property owners with multiple mortgages, are finding it generates effective returns of 4% or more when mortgage spend is high enough relative to regular card spend. The card does not earn rewards on tax payments, requires a minimum spend ratio to unlock mortgage points, and involves more active management than a flat-rate card. For members with the right profile, it is compelling. For members without significant mortgage payments, the case is weaker.

Robinhood Gold entered at 4% primary and 6% carried. At 3% back on all purchases with a $5/month Robinhood Gold membership requirement, it offers one of the highest flat cash back rates available. Several members in the thread describe directing the cash back straight into investment accounts, treating it as a passive savings mechanism. The main limitations are a waitlist and lower credit limits than established premium cards.

Coinbase One sits at 2% primary and 4% carried. It offers 4% back up to $10,000 per month with qualifying crypto holdings. Members who are already active Coinbase users find it a natural complement; members without existing crypto exposure typically find the setup overhead not worth it.

For members interested in exploring these cards, the Long Angle community has active threads with members sharing real-world results.

Frequently Asked Questions

What credit cards do high-net-worth individuals most commonly use?

Based on a June 2026 Long Angle poll of 564 members, American Express Platinum is the most common primary card (25%), with Chase Sapphire Reserve close behind at 24%. When asked which cards they carry, Amex Platinum leads at 50% and Chase Sapphire Reserve sits at 46%. Most members who hold one also hold the other, using them for different spending categories.

Is the Amex Platinum worth $895 a year?

It depends on how actively a member engages with its credits. The card offers over $3,500 in stated annual benefit value across hotel credits, Resy dining, entertainment subscriptions, Uber Cash, Equinox, CLEAR+, Oura Ring, lululemon, and lounge access. Members who travel frequently and use those credits consistently typically come out ahead. Members who travel occasionally and find the credits inconvenient to activate may not. Some members cover the fee entirely through the Morgan Stanley Annual Engagement Bonus program, which requires a qualifying Morgan Stanley relationship.

Do high-net-worth individuals prefer cash back or travel points?

Both are well-represented in the 2026 poll. Members who travel internationally and have schedule flexibility to use transfer partners often prefer points, where business class redemptions can produce 5 to 10 cents per point in effective value. Members who value simplicity and consistency prefer cash back. Several members in the 2026 thread described migrating from a complex points system toward a flat-rate cash back card as their time became more constrained. The right choice is a function of behavior, not net worth.

What changed with the Bank of America Preferred Rewards program in 2026?

As of May 2026, the Platinum Honors tier, which previously provided a 75% cash back bonus bringing the effective rate to 2.625%, now requires $1M or more in qualifying Bank of America and Merrill accounts, up from the prior $100K threshold. Members who held qualifying assets below $1M will see their bonus rate reduced. The change takes effect based on each member's program anniversary date, with a six-month transition period beginning May 26, 2026.

What is the best credit card for someone who does not want to think about it?

A flat-rate cash back card with no category tracking is the most common answer among Long Angle members who prioritize simplicity. Options in that category include the Robinhood Gold card (3% flat, requires $5/month Robinhood Gold membership), Bank of America Unlimited Cash Rewards (1.5% base, up to 2.625% with qualifying Merrill assets), and the Fidelity Rewards Visa (2% flat, carried by 12% of members in the 2026 poll). For members who travel occasionally and want one card that does most things well, Chase Sapphire Reserve comes up frequently as the simplest premium option.

Should high earners use more than one credit card?

The 2026 poll suggests the answer is yes for most. Amex Platinum and Chase Sapphire Reserve are each carried by roughly half of members, and most who have one have the other. Beyond two, the incremental value typically does not justify the added complexity. Members who run more than two cards tend to have a specific reason: a dedicated business card for advertising spend, an airline co-branded card at a hub they use frequently, or a mortgage-specific card like Bilt Palladium.

What credit cards are Long Angle members moving toward in 2026?

The 2026 poll shows Bilt Palladium (5% primary, 7% carried) and Robinhood Gold (4% primary, 6% carried) entering member wallets for the first time since 2024. Bilt Palladium is most compelling for members with large mortgage payments on rental properties or multiple homes. Robinhood Gold appeals to members who want a simple high-rate cash back card and are already Robinhood users. The Coinbase One card (4% up to $10K/month) is gaining ground among members with active crypto holdings.

Why do so many Long Angle members carry both Amex Platinum and Chase Sapphire Reserve?

The two cards complement each other without overlapping. Amex Platinum leads on direct airline bookings (5x), Centurion Lounge access, and lifestyle credits. Chase Sapphire Reserve leads on hotels booked directly (4x), dining (3x), and flexibility through the Chase Ultimate Rewards ecosystem. Members who split spend across both typically earn more than they would on either card alone, with the total annual fee offset by the credits each card provides. The thread discussion confirms this pairing is the most common deliberate card strategy among Long Angle members.

The Bottom Line

The best credit card for a high-net-worth individual is the one that fits their behavior. A member who travels internationally several times a year and is willing to manage a points system can generate substantial value from the Chase Sapphire Reserve or Amex Platinum, and most members who want both end up with both. A member who wants one card that works everywhere and sends the rewards straight to an investment account may be better served by a flat cash back option. Both are valid.

What shifts at higher wealth levels is the cost of complexity. When time is genuinely constrained, a card setup that requires monthly attention to credits, categories, and transfer windows has a real cost that does not show up in the points math. The members who are happiest with their setup tend to have picked something that fits their life and stopped optimizing.

Long Angle members regularly share what they're using, what changed their minds, and what they've stopped using. If you're building or rethinking your card setup, that conversation is worth joining.

Long Angle members regularly share what they're using, what changed their minds, and what they've stopped using. If you're building or rethinking your card setup, that conversation is worth joining.

Long Angle members receive preferential terms across a vetted set of financial product partners, including direct indexing tools, pledged asset lines, and banking products, through Long Angle Partnerships.

More from Long Angle

Beyond Wealth Newsletter

Long Angle's free weekly newsletter covering wealth management, investing and life at the intersection of money and ambition. Subscribe »

Navigating Wealth Podcast

The Long Angle podcast. Founders and executives on the financial and personal decisions that matter most. Listen »