High-Net-Worth Asset Allocation in Real Estate

Written By: Scott Nixon

Updated June 2026

2026 High-Net-Worth Asset Allocation Report

See how investors with an average net worth of $17M are allocating across public equities, private markets, real estate, bonds and cash. Based on benchmark data from 230+ respondents.

Real estate allocation decisions for high-net-worth investors are rarely about percentages. They are about which vehicles carry the risks you understand, which ones are priced honestly, and whether the rate environment you are entering favors the structure you are choosing. Getting those questions wrong is more expensive than being one or two points off on an allocation target.

How much of a high-net-worth portfolio should be in real estate? High-net-worth investors typically allocate 10-15% of their portfolios to real estate, though the right figure depends on wealth stage, liquidity needs, and which vehicles you choose. Public REITs, private equity funds, and real estate secondaries carry meaningfully different risk profiles and valuation mechanics. In the current rate environment, those distinctions matter more than the allocation percentage itself.

Key Takeaways

Long Angle member portfolios show real estate at approximately 11% on average, combining home equity and investment real estate

Public REITs have repriced significantly since 2021 — some sectors now trade at implied cap rates of 8-9%, reflecting a more realistic entry point than private equivalents

Non-traded private REITs carry valuation risk that public markets have already priced in; the BREIT situation illustrates how DCF-based models can obscure the impact of rising cap rates

LP-led real estate secondaries offer material discounts — often 20% or more — and a margin of safety that direct investing does not; GP-led secondaries typically trade near NAV and carry incentive misalignment worth understanding before committing

Small and mid-market real estate debt funds yielding 10-12% compete directly with institutional BDCs and mortgage REITs, which offer comparable yields with better teams, greater diversification, and public market liquidity

2026 may present selective buying opportunities in private markets as loan maturities create forced sellers; patient capital with conservative underwriting is better positioned than generalist allocators chasing yield

Table of Contents

How Much of My Portfolio Should Be in Real Estate?

Financial advisors have traditionally recommended allocating 20-30% of an investment portfolio to real estate for its income potential and long-term capital appreciation. Long Angle's annual asset allocation research shows members averaging roughly 11% across home equity and investment real estate — lower than that range, and reflective of investors who are also allocating meaningfully to private equity, private credit, and public markets. The right allocation is not a target. It is a residual of what you actually believe about returns, liquidity, and risk across your full portfolio.

The rate environment makes this question harder than it looks. The Federal Reserve cut rates 175 basis points through 2025, but the 10-year treasury — which broadly tracks real estate financing rates — has not followed, hovering above 4% since late 2022. Part of the sustained pressure comes from global fiscal spending increasing worldwide debt supply, pushing up yields regardless of domestic monetary policy. CBRE consensus data forecasts the 10-year declining over the next several quarters, which would relieve pressure on cap rates across sectors. Until that happens, the rate environment continues to favor buyers over sellers and patience over speed.

CBRE also notes that commercial real estate has not been this competitively priced on a relative basis in several years, with cap rate expansion across office, industrial, retail, multifamily, and hotel sectors since 2022. That creates a more realistic entry point than existed in 2020-2022, when private market valuations diverged from economic reality. Investors who came in at peak valuations with floating-rate debt are the ones now creating opportunity for those with patient capital.

For more on how high-net-worth investors approach overall allocation decisions, see how Long Angle members allocate across asset classes.

Beyond Wealth Newsletter

Weekly perspectives on wealth, investing, and the decisions that matter after the financial ones get easier. Read by founders, investors, and executives navigating the same questions covered in this post.

How Much of My Retirement Should Be in Real Estate?

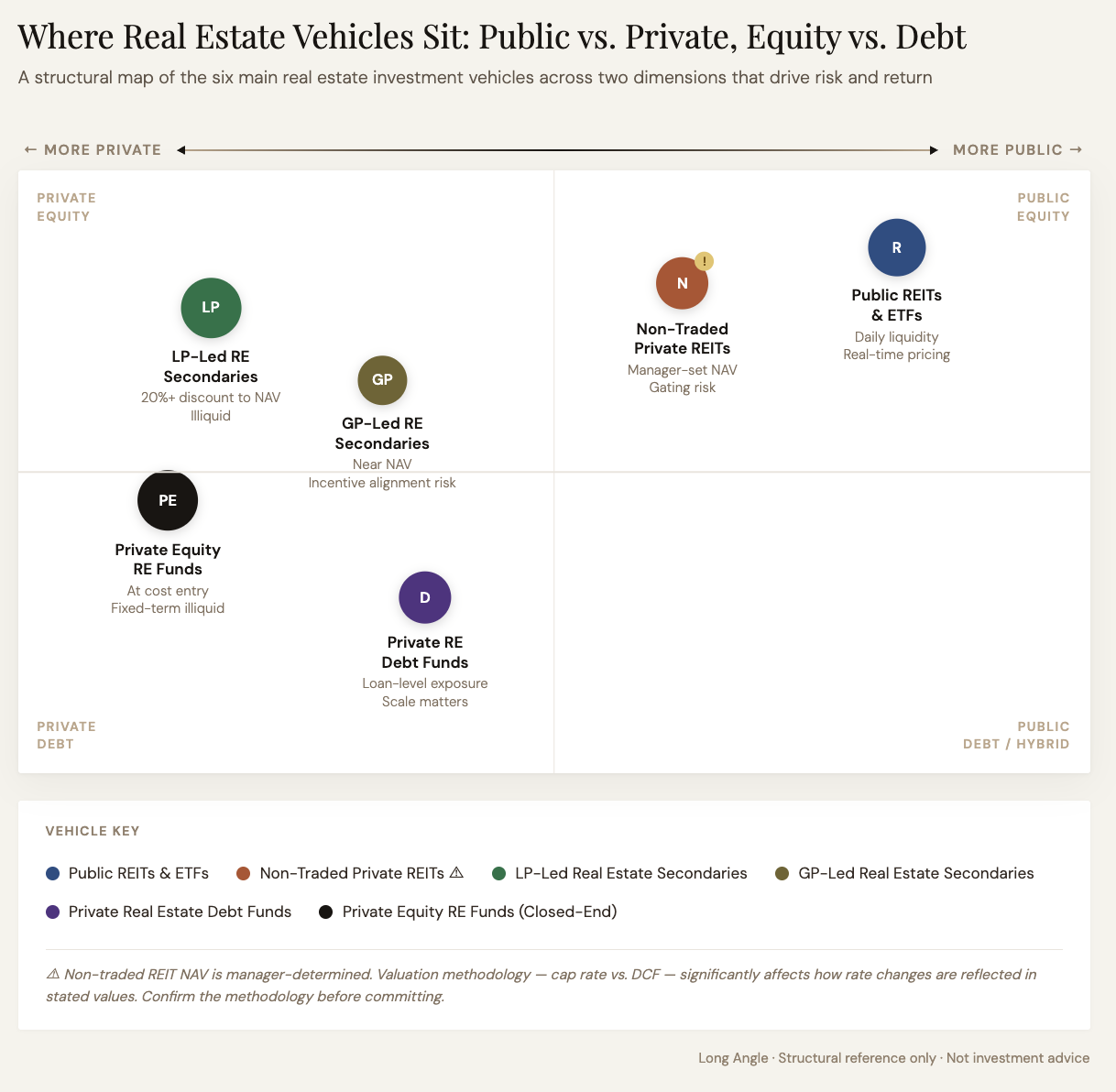

Not all real estate vehicles carry the same risk. Understanding how each is structured — and how each is priced — matters more at this wealth level than the allocation percentage itself.

Public REITs and real estate ETFs trade on public exchanges and offer the rare combination of real-time pricing, liquidity, and income through dividends. VNQ declined approximately 30% from its December 2021 peak as interest rates rose sharply — a correction that private market equivalents have not fully reflected. Some retail REITs now trade at implied cap rates of 8-9%, representing a more honest valuation than private alternatives in the same sector. The tradeoff is volatility: public REITs amplify rate sensitivity far more than private vehicles, which means they can look unattractive in rising rate environments and more attractive once rates stabilize.

Non-traded private REITs — including large vehicles like BREIT and SREIT — offer semi-liquidity when not gated and broader diversification than direct ownership. The core risk is valuation methodology. During the rate-rising cycle, some large non-traded REITs used discounted cash flow models rather than cap rate models, which masked the impact of rising cap rates on asset values. That disconnect between model and market created conditions for gating and investor redemption pressure. Smaller private REITs carry similar risk with less scrutiny. The question is not just whether the underlying assets are good — it is whether the stated NAV reflects the same assumptions public markets are using.

Private real estate secondaries are one of the more structurally sound entry points in the current environment. Wide bid-ask spreads have suppressed transaction volume: sellers have no incentive to exit because their properties are generally operating adequately, they either have long-term fixed debt or have received lender extensions, and they are not pressured to reprice. This dynamic creates good secondary market conditions — LPs need liquidity and GPs cannot sell. LP-led secondaries enter at material discounts, often 20% or more, providing a margin of safety that direct investing does not. GP-led secondaries are a different instrument: they typically trade near NAV at 0-5% discounts and require more scrutiny of incentive alignment when the GP is on both sides of the transaction.

Private real estate debt funds range from small hard money lenders to large institutional credit managers, and the difference matters. Smaller funds offering 10-12% net returns compete directly with institutional BDCs — middle market direct lending funds — which offer comparable yields with better underwriting, larger teams, greater diversification, and public market liquidity. Large institutional managers also have more experience managing workouts when loans deteriorate, which is when the quality of the team becomes most apparent.

Private equity real estate funds (closed-end) enter at cost, which removes the NAV pricing problem that affects non-traded REITs. Everyone in the fund comes in at cost, so there are no pricing shenanigans from investors entering at different valuations. With select asset classes now showing 25-30% corrections from 2022 peak valuations, patient capital has more opportunities than at any point in the prior three years.

Real estate crowdfunding and syndications enable investors to participate in specific projects or portfolios at lower minimums. Quality varies significantly by sponsor and structure. For a more detailed look at how syndications work, see how real estate syndication works for accredited investors.

Real Estate Vehicle Comparison

| Vehicle | Liquidity | Valuation Transparency | Typical Entry vs. NAV | Income / Growth | Accreditation |

|---|---|---|---|---|---|

| Public REITs / ETFs | Daily | Real-time market pricing | Market price (can trade at discount or premium) | Both, varies by type | Not required |

| Non-traded private REITs | Limited (gating risk) | Manager-set NAV* | At stated NAV | Income-oriented | Typically yes |

| LP-led RE secondaries | Illiquid (fund term) | Fund-level, periodic | 20%+ discount to NAV | Growth + income | Yes (QP common) |

| GP-led RE secondaries | Illiquid (fund term) | Fund-level, periodic | 0-5% discount to NAV | Varies | Yes (QP common) |

| Private RE debt funds | Illiquid to semi-liquid | Loan-level, periodic | At par (originated) | Income-oriented | Yes |

| Private equity RE funds (closed-end) | Illiquid (fixed term) | At cost on entry; periodic thereafter | At cost (all investors equal) | Growth-oriented | Yes (QP common) |

*Non-traded REIT NAV is manager-determined. Methodology — cap rate vs. DCF — significantly affects how rate changes are reflected in stated values.

How Are High-Net-Worth Individuals Investing in Real Estate?

The most useful signal on where serious allocators are deploying — and where they are staying on the sidelines — comes from operators actively in specific markets. The picture varies considerably by sector.

Multifamily has seen pricing corrections of 25-30% from 2022 peak valuations in oversupplied markets, particularly Sun Belt metros that experienced rapid cap rate compression. MSCI data from mid-2025 showed multifamily distress rising over 70% year-over-year. For buyers with patient capital and genuine operating capacity, markets with real housing demand and supply constraints are beginning to offer realistic entry prices. Suburban affordable housing is attracting attention from operators who can manage without a joint venture premium. Markets like DFW, Austin, and Phoenix are going through cost basis resets that create selective opportunities for buyers with long time horizons.

Hotels posted negative RevPar growth in 2025 for the first time since 2020, with insurance and labor costs compressing margins. Institutions tired of the asset class are creating exit opportunities for smaller regional operators who can underwrite at current economics rather than pre-pandemic assumptions. Deal quality and viability remain highly market-dependent.

Self-storage, manufactured housing, and RV parks have seen buyers outpacing sellers even as cap rates rose, suggesting investors believe cash flow durability holds across cycles. Positive leverage remains difficult to find — the spread between cap rates and financing costs is still compressed in many markets. Operators in these sectors generally expect the best distressed opportunities to surface in the second half of 2026 as loan maturities arrive and extend-and-pretend dynamics run out of runway. For a detailed look at the supply and demand dynamics specific to these sectors, see manufactured housing and self-storage investing.

Build-to-rent continues to attract interest due to the ongoing US housing shortage. Investors in this format report stronger deal flow than traditional multifamily in some submarkets, with fewer distress-driven dynamics complicating underwriting.

Where do serious allocators compare notes on private real estate vehicles, secondary discounts, and which managers are worth the fees?

Long Angle is a vetted community where members share what they are deploying, what they passed on, and what the diligence actually showed. The environment is solicitation-free — no placement agents, no commissions. When a member recommends a fund or flags a valuation problem, it is because they have skin in the game.

Best Practices for High-Net-Worth Portfolio Allocation

A few principles tend to separate real estate allocation decisions that hold up over time from ones that look good on paper and deteriorate in practice.

Understand the valuation methodology before committing. In direct ownership and closed-end funds, assets are held at cost or appraised periodically. In non-traded REITs, the NAV is manager-determined and the methodology matters. The difference between a cap rate model and a DCF model is not academic — it is the difference between an honest price and a flattering one during periods of rate stress.

Distinguish LP-led from GP-led when evaluating secondaries. LP-led secondary transactions offer discounts driven by the LP's need for liquidity, independent of the underlying asset quality. GP-led transactions are initiated by the GP, often involve less price discovery, and require more scrutiny of incentive alignment. Both can make sense in specific situations, but they are not interchangeable.

Compare yield on a risk-adjusted basis, not in isolation. A small real estate debt fund offering 12% net competes with institutional BDCs offering similar yields with better teams, more diversification, and public market liquidity. The 12% is not a premium for complexity; it is often compensation for opacity and limited workout capacity.

Think in terms of asset location across the full portfolio. Passive depreciation from real estate equity positions can offset passive income from other sources. For high W-2 earners, direct real estate equity — not debt — is typically where the depreciation benefit lives, and matching it to the right income offset requires thinking across the full portfolio. After-tax return is the number that matters.

Be deliberate about liquidity. Real estate is less liquid than most other asset classes. The right mix of public REITs, private funds, and direct ownership depends partly on when you might need access to capital and whether you can tolerate gating risk during market stress.

Align investments with goals before selecting vehicles. Whether the primary objective is cash flow, diversification, capital appreciation, or tax efficiency should determine which vehicle to use — not the other way around. For more on how commercial real estate fits into a broader investment portfolio, see incorporating CRE into a broader portfolio.

High-Net-Worth Real Estate Diversification

Diversification in real estate means more than owning multiple properties. It means distributing exposure across geographies, sectors, investment vehicles, development stages, and income objectives in ways that reduce correlated risk.

Geographic diversification protects against local market downturns — multifamily oversupply in one Sun Belt metro does not affect manufactured housing in the Midwest the same way. Sector diversification spreads exposure across residential, commercial, industrial, retail, and specialty property types that respond differently to economic cycles. Vehicle diversification across direct ownership, REITs, private equity funds, and secondaries gives access to different liquidity profiles, return drivers, and valuation methodologies.

The LP-led vs. GP-led distinction is also a form of diversification. LP-led secondaries offer discounted entry driven by liquidity needs independent of asset performance. GP-led secondaries are structurally different. Knowing which you own and why matters when market conditions change.

Income vs. growth focus matters too. Some real estate investments provide steady income through rental yields; others offer potential for capital appreciation. A portfolio oriented entirely toward one or the other tends to underperform across full market cycles compared to a deliberate mix tied to actual income needs.

Frequently Asked Questions

How much of a high-net-worth portfolio should be in real estate?

There is no universal answer, but Long Angle's benchmark data shows members averaging roughly 11% across home equity and investment real estate — lower than the 20-30% range often cited by advisors. That figure reflects investors who are also allocating to private equity, private credit, and public markets. The right allocation is the one that fits within your full portfolio given your liquidity needs, tax situation, and return objectives.

What is the difference between LP-led and GP-led real estate secondaries?

LP-led secondaries occur when a limited partner needs liquidity and sells their fund stake at a discount — typically 20% or more off NAV — driven by their own financial needs rather than the performance of the underlying assets. GP-led secondaries are initiated by the fund manager, often to extend the fund's life or provide liquidity to some LPs. They tend to trade closer to NAV, at 0-5% discounts, and require more scrutiny of incentive alignment because the GP is on both sides of the transaction.

Why are non-traded private REITs riskier than they appear?

Non-traded REITs determine their own NAV, and the methodology matters significantly. Some large vehicles used discounted cash flow models during the rate-rising cycle rather than cap rate models, which masked the impact of rising rates on asset values. The result was a stated NAV that did not reflect what public markets were pricing for comparable assets. Investors who relied on that NAV for allocation or redemption decisions were working from a misleading number.

How do real estate debt funds compare to BDCs for yield-seeking investors?

Both offer yield in the 9-13% range, but institutional BDCs generally offer better underwriting, larger and more experienced teams, greater diversification across borrowers, and public market liquidity. Small and mid-market real estate hard money funds may offer similar headline yields, but limited workout capacity and higher opacity at the smaller end of the market reduce the risk-adjusted appeal. For most investors, institutional credit managers represent a better trade-off at comparable yield levels.

Which real estate sectors offer the most opportunity in 2026?

Multifamily in supply-constrained markets is showing realistic entry prices after 25-30% corrections from 2022 peaks. Build-to-rent continues to attract interest due to the US housing shortage. Self-storage and manufactured housing may see more distressed opportunities in the second half of 2026 as loan maturities arrive. Hotels are creating regional buying opportunities as institutions exit and lender-forced sales come to market.

What is a cap rate and why does it matter for real estate allocation decisions?

A cap rate (capitalization rate) is calculated by dividing a property's net operating income by its current market value. It functions as a yield measure for real estate. When interest rates rise, cap rates tend to rise too — which means asset values fall to maintain the spread over risk-free rates. The disconnect between how quickly public REITs repriced and how slowly private real estate valuations adjusted is the core risk in non-traded private vehicles. Whether a vehicle's stated value reflects current cap rate assumptions is one of the most important questions an investor can ask.

How does real estate fit into an overall alternative investment allocation?

Real estate typically functions as an income-generating and inflation-sensitive component of the alternatives sleeve, distinct from private equity (growth-oriented, longer duration, less cash flow) and private credit (higher in the capital stack, more protective). At the 10-15% range that Long Angle members tend to show, real estate sits alongside meaningful allocations to private equity and private credit rather than dominating the alternatives sleeve. The right balance depends on how each component behaves in the macro scenarios most relevant to your portfolio.

The most useful real estate conversations are not in research reports.

Long Angle members discuss specific vehicles, specific managers, and specific mistakes across the full spectrum of real estate investing — from public REITs to LP-led secondaries to private equity funds. When a member flags a valuation problem, passes on a named fund, or shares what they actually closed on and at what discount, that signal travels through a community of 8,000+ vetted peers who have no motive other than getting it right.

More From Long Angle

Beyond Wealth Newsletter

Long Angle's free weekly newsletter covering wealth management, investing and life at the intersection of money and ambition. Subscribe »

Navigating Wealth Podcast

The Long Angle podcast. Founders and executives on the financial and personal decisions that matter most. Listen »