Sudden Wealth and How to Manage It: The New to Wealth Checklist

Written By: Chris Bendtsen

Compare Notes With Peers Navigating the Same Decisions

See how high-net-worth households use professional services, what they pay, and how satisfaction stacks up across advisors, estate planners, tax professionals, and more.

Long Angle's New to Wealth Checklist is a guide to managing sudden wealth, covering the five domains that matter most after a liquidity event, exit, equity vest, or inheritance. The checklist names the foundational moves, the key concepts every high-net-worth individual should know, and the recommended next step for each.

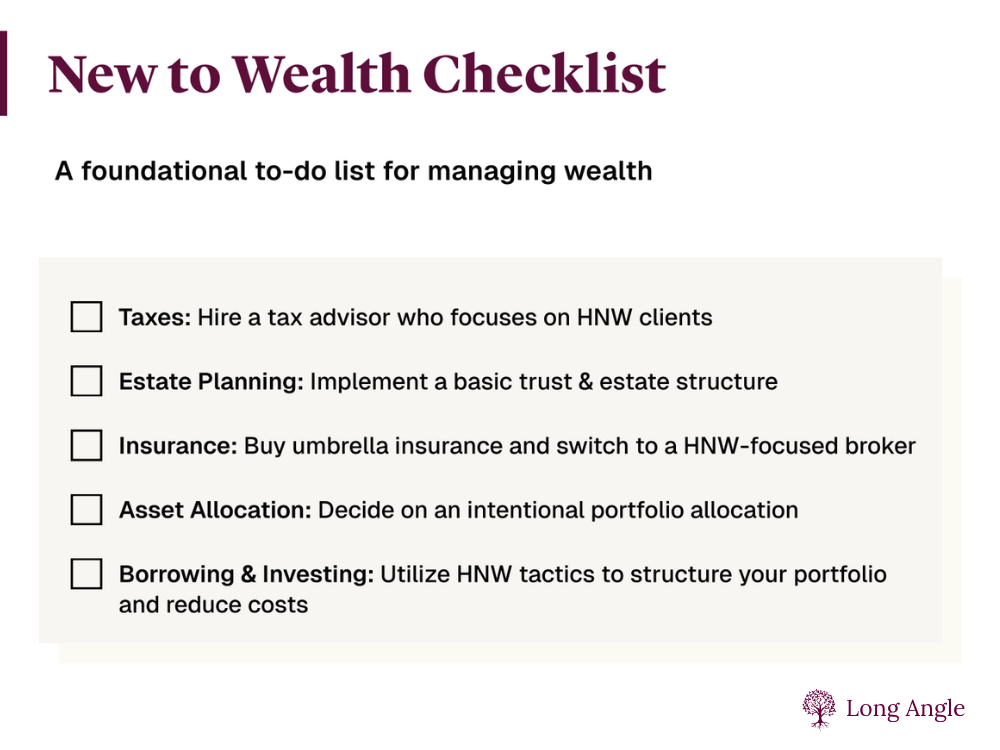

The Five Foundational Moves for Managing Wealth

Managing sudden wealth requires five foundational moves in the first year: hire a tax advisor focused on high-net-worth clients, implement a basic trust and estate structure, buy umbrella insurance through a HNW-focused broker, set an intentional portfolio allocation, and use HNW-specific borrowing and investing tactics to reduce costs. Each move prevents irreversible mistakes that compound over time.

Key Takeaways

A standard accountant files your taxes. A high-net-worth tax advisor builds proactive strategy around capital gains timing, equity compensation, QSBS exclusions, and business entity structure.

A basic trust and estate plan (will, powers of attorney, revocable living trust) prevents probate exposure, avoids unnecessary estate tax, and resolves guardianship.

Umbrella insurance from a HNW carrier (Chubb, AIG, Berkley One, or PURE) through an independent broker is one of the highest-ROI purchases in the checklist. Most HNW households carry $5 to $10 million in coverage for a few thousand dollars per year.

Intentional asset allocation across public equities, fixed income, real estate, private markets, and alternatives is the foundation. Broader access becomes available as wealth grows.

HNW borrowing and investing tactics like portfolio-based lending and box spreads, direct indexing, Private Placement Life Insurance, and mega backdoor Roth contributions can save several percentage points per year in costs and taxes.

New to Wealth Checklist

Estate Planning: Implement a Basic Trust and Estate Structure

Insurance: Buy Umbrella Insurance and Switch to a HNW-focused broker

Asset Allocation: Decide on an Intentional Portfolio Allocation

Borrowing and Investing: Utilize HNW Tactics to Structure Your Portfolio and Reduce Costs

This checklist will make sure you have the right foundations in place. Each area is explored in more detail with recommended next steps below.

Taxes

Hire a tax advisor who focuses on HNW clients

A standard accountant files your taxes. A high-net-worth tax advisor builds a proactive tax strategy around your entire financial picture: minimizing liability, maximizing deductions, and treating tax as a year-round planning consideration.

Key strategies include:

Capital gains management: harvesting losses, deferral strategies, and timing gains across years.

Tax code provisions: QSBS exclusions, charitable vehicles, opportunity zones, and real estate depreciation.

Equity comp planning: ISOs, NSOs, RSUs, AMT exposure, and exercise timing.

Business entity structuring: LLCs, S-corps, and other vehicles to minimize tax liability.

Income timing and deferral: controlling when you recognize income to manage the effective rate.

Multi-state and international tax exposure.

Next step: Become a Long Angle member and book a call with our vetted tax partner for planning and filing.

We evaluated dozens of member-nominated tax advisors and narrowed the list to finalists based on HNW focus, nationwide breadth, and expertise with complex situations. We then ran a pilot with more than 20 Long Angle members across multiple firms that resulted in a clear winner. Since then, more than 100 members have retained our partner with overwhelmingly positive feedback.

Estate Planning

Implement a basic trust and estate structure

Neglecting to implement a basic estate plan may leave assets exposed to probate, trigger unnecessary estate taxes, and create ambiguity around guardianship.

Components include:

Basic documents: will, durable power of attorney, medical power of attorney, and healthcare directive.

Revocable living trust: a flexible trust you control during your life that avoids probate, protects privacy, and simplifies distribution to heirs. Most start here, then add irrevocable structures.

Irrevocable trusts: more complex structures that provide asset protection and estate tax reduction. Your attorney may recommend SLATs, GRATs, IDGTs, DAPTs, or CRUTs.

Next step: Ask trusted contacts for an estate attorney recommendation.

Long Angle is currently exploring options to evaluate estate planning attorneys on behalf of the membership.

Beyond Wealth Newsletter

Weekly perspectives on money, meaning, and the decisions that come after the financial ones get easier. Read by founders, executives, and investors navigating the same questions covered in this post.

Insurance

Buy umbrella insurance and switch to a HNW-focused broker

Umbrella insurance is an inexpensive way to protect against catastrophic financial loss. HNW insurance provides much better service for only marginally more cost.

Umbrella policy: a liability policy that sits above home and auto, protecting assets from lawsuits exceeding standard policy limits. Most Long Angle members buy $5–10 million of coverage, paying a few thousand dollars per year.

HNW carriers: Chubb, AIG, Berkley One, and PURE pay agreed value on homes, cover high-value vehicles, offer higher liability limits, and provide concierge claims service.

Independent broker: unlike a captive agent representing a single carrier, a broker will compare options across multiple carriers to find the best price/coverage combination. This is especially important for HNW coverage.

Next step: Apply for Long Angle membership to gain access to:

Long Angle’s Group Umbrella Policy: Up to $10M in coverage. Easy, online enrollment with no underwriting required.

Our vetted insurance broker partner for home, auto, umbrella, and more.

We worked with a HNW insurance carrier to structure a group umbrella plan for members with no underwriting, no agent required, and coverage in minutes. For the broker, we personally tested more than 10 options. Our selected partner stood out for their tech-enabled onboarding, rapid response time, and attention to detail (catching policy details that other brokers missed). Over 700 Long Angle members have leveraged these resources.

Asset Allocation

Decide on an intentional portfolio allocation

As your wealth grows, so does your access to asset classes. A broader mix allows you to better diversify and align your target allocation with your specific goals.

Core asset classes:

Public equities: stocks and index funds

Fixed income: bonds, Treasuries, and munis

Real estate: direct ownership, REITs, and private RE funds

Private markets: private equity, venture capital, and private credit

Alternatives: hedge funds, commodities, energy, infrastructure, precious metals, crypto, collectibles, art, and royalties

Key considerations for each:

Return potential

Volatility and risk

Cash flow and liquidity needs

Complexity and time commitment

Next step: Identify your primary financial goal (e.g., growth, income, wealth preservation) and determine the level of volatility you’re willing to accept in pursuit of returns. Then, select asset classes that align with these priorities.

Long Angle is exploring partnerships with flat-fee RIAs to help members with longterm asset allocation planning.

Looking for a peer community that goes beyond the portfolio?

Long Angle is a private, vetted community of high-net-worth entrepreneurs and professionals comparing notes on everything from estate planning to post-exit identity, without solicitation.

Borrowing and Investing

Utilize HNW tactics to structure your portfolio and reduce costs

Borrowing against stocks at low rates: use your stock portfolio as collateral to fund large expenses without selling assets or triggering taxes. Setting this up properly (box spreads or a cost-competitive broker) can be the difference between paying ~5% and ~10% annual interest.

Direct indexing: buying the stocks in an index individually rather than owning an index fund. This delivers similar returns for comparable fees, while providing significant tax savings.

Private Placement Life Insurance (PPLI): buying assets through a PPLI structure virtually eliminates taxes on investment income and capital gains. For investments that generate significant taxable income like private credit and hedge funds, this tax savings can exceed 5% per year, which significantly outweighs the fees and complexity of the PPLI vehicle.

Mega backdoor Roth IRA: if your employer's 401(k) allows after-tax contributions and in-plan Roth conversions, you may be able to contribute $72,000 or more each year into a Roth account. That money grows tax-free and is withdrawn tax-free, without RMDs.

Next steps: Join Long Angle to access tactical borrowing and investing products with preferential pricing:

Explore portfolio-based lending through your brokerage or via Long Angle partners at lower rates.

Learn more about direct indexing with Long Angle’s vetted partner.

Become a member and express interest in a group PPLI product.

Check if your employer’s 401(k) plan allows after-tax contributions and in-plan Roth conversions.

Frequently Asked Questions

What should I do first when I come into sudden wealth?

The most important first step is to resist the urge to make major financial decisions immediately. Give yourself a cooling-off period, ideally 3 to 6 months, while you assemble a team of professionals. That means hiring a high-net-worth tax advisor, an estate planning attorney, and an insurance broker who specializes in wealthy clients. Use this time to understand the tax implications of your new wealth, get a clear picture of your net worth, and start building a long-term financial plan before making large purchases or investments.

How long does it take to put the full new to wealth checklist in place?

The full checklist takes 12 to 18 months to implement well. The first 30 days are for the cooling-off period and hiring a high-net-worth tax advisor and umbrella insurance broker. Within 90 days, basic estate planning documents and a revocable living trust should be in place. Within 6 months, an intentional asset allocation across public and private markets should be set. The advanced tactics, including direct indexing, Private Placement Life Insurance, mega backdoor Roth contributions, and irrevocable trust structures, typically come within the first 12 months as the foundation stabilizes. Those who try to do everything at once usually end up redoing parts of the work.

Do I really need a trust, and when should I set one up?

Yes, for most people with significant wealth, a trust is one of the most valuable tools you can put in place. A revocable living trust avoids probate, keeps your affairs private, and simplifies how assets are distributed to heirs. It also gives you full control during your lifetime. The right time to set one up is as soon as possible after achieving significant wealth. Beyond that, your estate attorney may recommend irrevocable structures (such as GRATs, SLATs, or IDGTs) to reduce estate taxes and protect assets. Waiting exposes your estate to unnecessary risk and cost.

How do high-net-worth individuals reduce their tax burden?

Tax planning for HNW individuals goes far beyond filing an annual return. Key strategies include capital gains management (harvesting losses, timing gains across years), equity compensation planning (ISOs, NSOs, RSUs, and AMT exposure), business entity structuring (LLCs and S-corps), and income deferral. More advanced tools include QSBS exclusions, opportunity zones, charitable vehicles, and Private Placement Life Insurance (PPLI), which can virtually eliminate taxes on investment income and capital gains. The key is working with a tax advisor who specializes in high-net-worth clients and treats tax as a year-round strategy, not an annual event.

What is umbrella insurance and how much coverage do I need?

Umbrella insurance is a liability policy that sits on top of your existing home and auto coverage, protecting your assets from lawsuits that exceed your standard policy limits. For high-net-worth individuals, it's one of the most cost-effective forms of asset protection available. Most people with significant wealth carry $5–10 million in umbrella coverage, which typically costs only a few thousand dollars per year. It's also worth switching from a standard insurance carrier to a HNW-focused one (like Chubb, AIG, PURE, or Berkley One), which offer agreed value coverage, higher limits, and concierge claims service, often for only marginally more in premiums.

How should I invest my money once I have significant wealth?

The answer depends on your primary financial goal (growth, income, or wealth preservation) and your tolerance for risk and illiquidity. High-net-worth individuals have access to asset classes beyond standard stocks and bonds, including private equity, venture capital, private credit, real estate funds, hedge funds, and alternative investments. The goal is an intentional allocation across these categories that matches your objectives. Strategies like direct indexing (owning index stocks individually for tax efficiency), portfolio-based lending (borrowing against your assets at low rates without triggering taxable events), and a mega backdoor Roth IRA can further optimize your portfolio. Start by defining your goals before selecting asset classes.

What is sudden wealth syndrome and how can it be avoided?

Sudden wealth syndrome is the pattern of psychological and behavioral difficulties that can follow a sudden increase in wealth: decision paralysis, isolation from old peer groups, identity disruption, guilt, and impulsive spending or investing. It is a recognized pattern across exit founders, inheritance recipients, and lottery winners, though the specific stressors differ by source. The most effective preventatives are practical: a 3 to 6 month cooling-off period before major financial decisions, a team of professionals hired in sequence rather than all at once, a community of peers who have navigated the same transition, and a written long-term plan that anchors decisions back to specific goals rather than emotion.

About Long Angle

Long Angle is a private community of high-net-worth investors who leverage their collective expertise and scale to access and underwrite institutional-quality alternative asset investments. Asset classes range from private equity, search funds, and private credit to secondaries, real estate, and venture capital.

Long Angle is a high-net-worth peer community, not a wealth manager. Members independently make their investment decisions on a deal-by-deal basis. They are treated as partners in every investment, with full transparency regarding the investment team's diligence and underwriting processes. All members receive equal access to negotiated fee discounts.

Membership is free but requires an interview with a current community member, as well as validation of investable assets. Apply Now »