Software vs. AI Q1 2026: SaaSpocalypse Examined

Long Angle's Software vs. AI Q1 2026 unpacks the SaaSpocalypse narrative that erased hundreds of billions in software market cap in early 2026. The paper covers the AI product launches and funding rounds that drove the selloff, the downstream pressure on private credit redemptions and private equity marks, and a data-driven look at SaaS fundamentals. We examine revenue growth, net revenue retention, Rule of 40, EBITDA margins, operating ratios, and ARR per employee to help investors assess what's noise and what's a real structural shift.

Contents

Access the Full White Paper Here

SaaSpocalypse: What's Happening?

The “SaaSpocalypse” refers to the sharp decline in market valuations of traditional software-as-a-service companies and a pessimistic outlook on their future business prospects. This narrative is driven by the emergence of AI agents capable of automating workflows that previously required enterprise software, presenting the possibility that SaaS businesses could be completely displaced or significantly weakened going forward.

The thesis had been building for over a year. As early as December 2024, Microsoft CEO Satya Nadella argued on the BG2 podcast that SaaS applications will "collapse" in the agent era, once AI agents take over the business logic layer. By early 2026, that thesis had moved from speculation closer to reality. The term SaaSpocalypse was coined by a Jefferies trader in February 2026 as markets began to price in the potential consequences of new AI products.

One of the main fears is that AI agents threaten the per-seat licensing model that has underpinned SaaS growth and business models for a decade. If enterprises deploy AI agents that reduce headcount, the number of software seats shrinks and with it the recurring revenue that justified high valuation multiples.

Software Selloff

Earnings growth for software and services companies in the S&P 500 was projected to accelerate in 2026 according to Bloomberg Intelligence: rising to 21% from 17% last year. So even though the fundamentals were solid and expected to strengthen, investors sold in response to the AI threat.

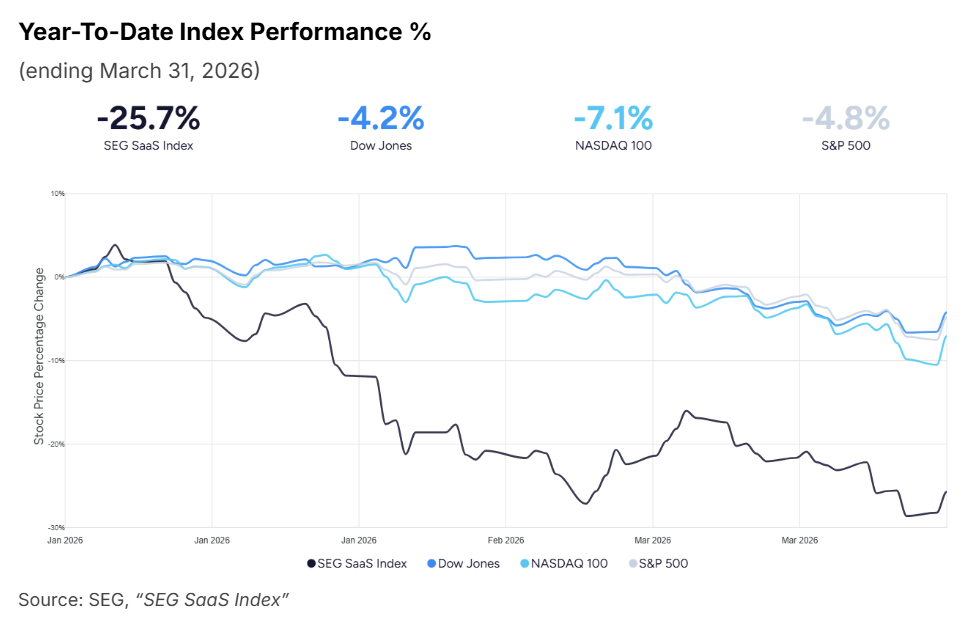

The declines in public software stocks have been severe. The SEG SaaS Index, which tracks more than 120 publicly traded software companies, is down 25.7% year-to-date (as of March 31, 2026). While IGV is often cited in the press as a representation of the software sector, its top two holdings are Palantir and Microsoft, which are likely better positioned to benefit from AI. We analyze the SEG SaaS Index throughout this paper to exclude those names.

It’s important to note that software stocks had begun to stabilize in late February, but broad market declines in March driven by the US and Israel conflict with Iran weighed on equities across all sectors. Thus, the year-to-date figures reflect both the AI-driven software selloff and the broader macro environment, and should not be read as a pure measure of software-specific disruption risk.

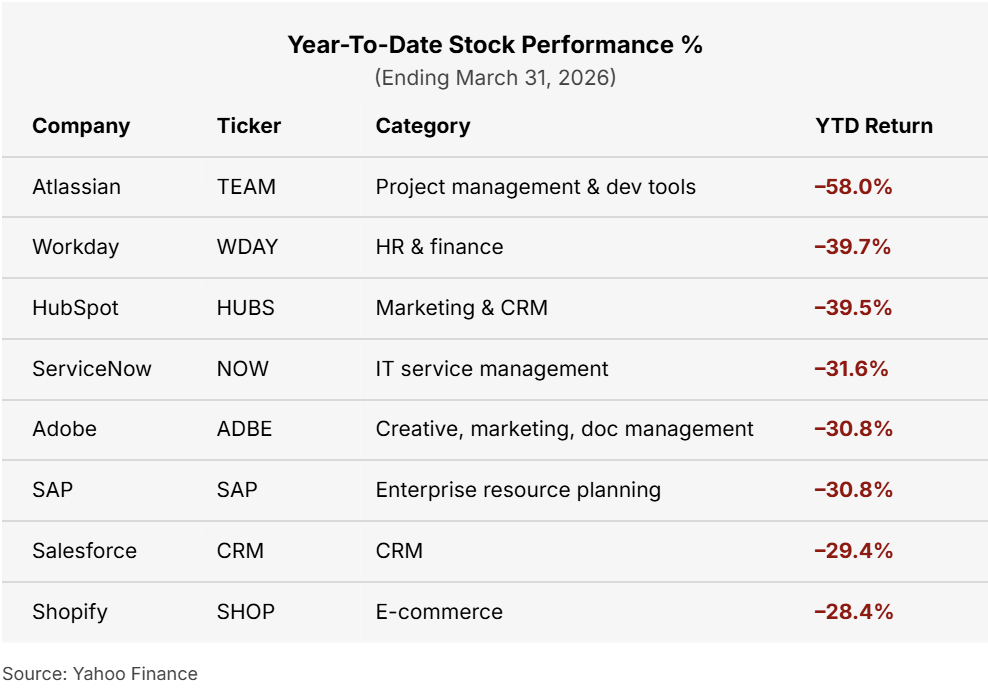

Even so, the declines among large, widely recognized software companies have been substantial. Most of the hardest-hit names are horizontal software platforms serving broad enterprise needs. The market believes their core functionality is at risk of being replicated by AI code generation tools. Atlassian's project management suite, HubSpot's marketing automation, and Workday's HR workflows are all products where an AI agent could, in theory, execute the same tasks without a per-seat license. Whether that replacement is imminent or technically feasible at scale remains unknown, but the market is pricing in the risk.

AI Funding Contrast

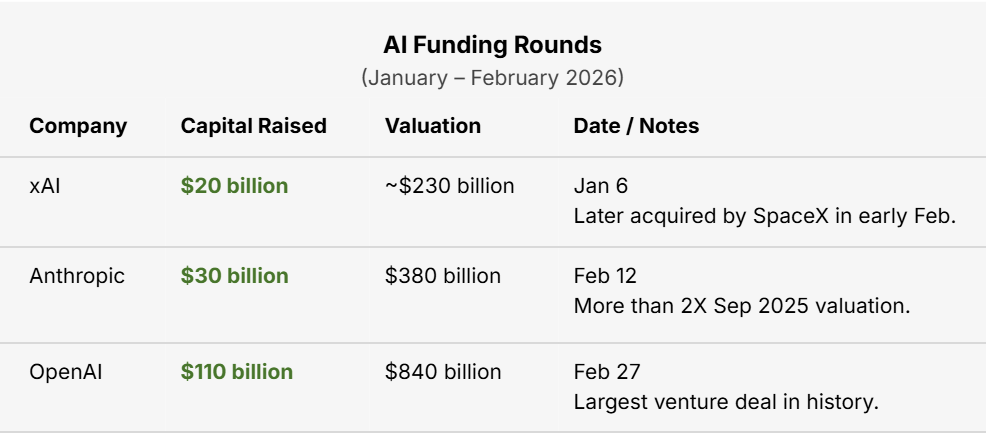

While software stocks were selling off, AI companies were raising capital at an extraordinary pace. In January and February, three major foundational model providers raised a total of $160 billion in venture funding—fueling the SaaSpocalypse narrative even further.

The bet on AI displacing software has been visible in the venture capital ecosystem well before the February 2026 selloff. AI startups have raised significant capital in the last few years based on two distinct theses:

AI specialists replacing SaaS incumbents in specific enterprise workflows.

AI build-your-own tools enabling companies to bypass packaged software entirely.

On the first front, private investors are betting that a purpose-built AI application can do the job of an incumbent SaaS product more efficiently, at lower cost, and without the per-seat pricing model. Harvey, an AI platform for legal research and contract analysis with an $11 billion valuation, directly competes with Thomson Reuters and LexisNexis. Sierra ($10 billion) and Decagon ($4.5 billion) are both AI-native customer service platforms competing in territory long owned by Salesforce Service Cloud and ServiceNow. Glean ($7.2 billion), an AI-powered enterprise search and knowledge management platform, could displace workflows currently handled by Salesforce, ServiceNow, and Microsoft 365.

The second vector may represent the more fundamental threat. Cursor, an AI coding platform valued at $29.3 billion, markets itself as a tool to 'develop enduring software at scale.' This means enterprises can build their own custom solutions rather than licensing them from vendors. Replit ($9 billion valuation) goes further: it allows non-technical users to build functional applications through conversational prompts with no developers required. The implication is that if a company can instruct an AI agent to build a custom CRM, a bespoke project management tool, or an internal legal workflow system in days rather than months, the value proposition of paying for packaged software weakens.

Private Markets Ripple

Private Credit

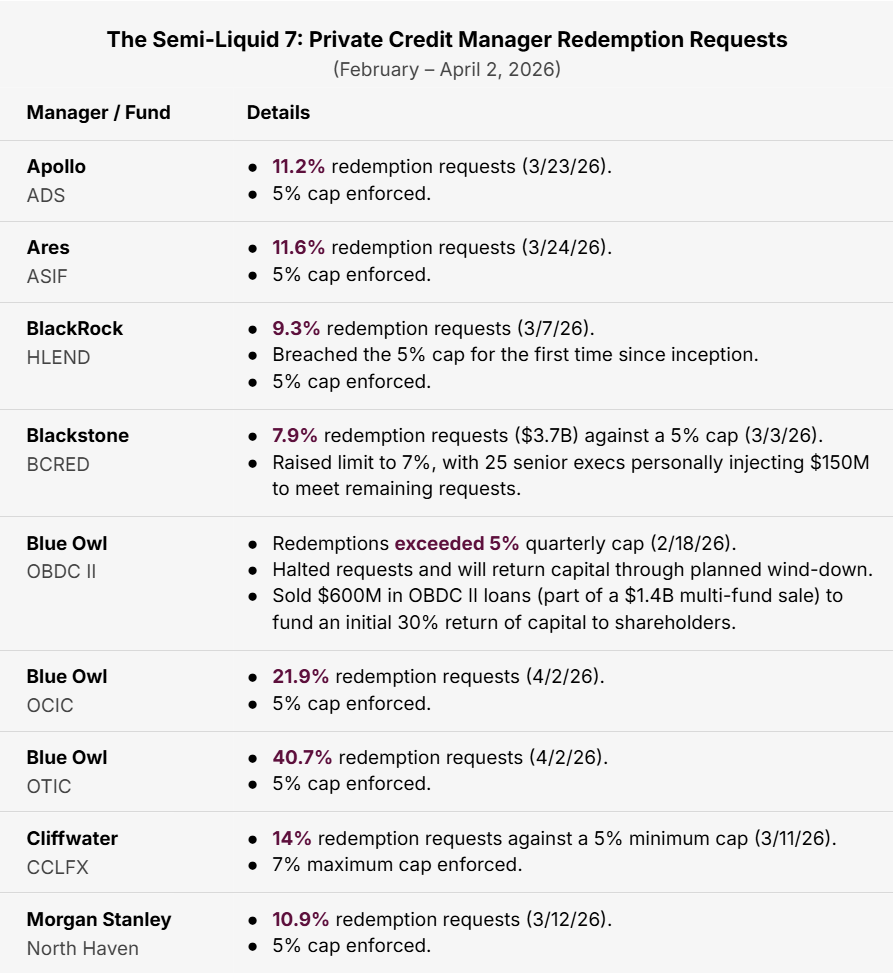

Within weeks, the software selloff moved to private markets. Investors sought to pull over $10 billion from private credit funds, driven by fears of over-exposure to software companies perceived as vulnerable to AI disruption. The concern is understandable as software has been a prominent sector in private credit business development company (BDC) portfolios for a decade. Barclays estimates roughly 20% of BDC portfolios industry-wide carry software exposure, approximately $100 billion in total.

Multiple private credit funds hit quarterly redemption caps in February and March from investors looking to exit. Whether the flood of redemptions represents genuine credit stress or a sentiment-driven overreaction remains to be seen. For a more detailed look at these events and the current health of the private credit market, see Long Angle's companion paper,Private Credit Perspectives Q1 2026: Signs of Stress or Sound Plumbing?

In early March 2026, JPMorgan marked down the value of software-collateralized loans held by private credit funds, effectively reducing how much those funds can borrow against their portfolios. Private credit funds commonly borrow from banks using their own loan portfolios as collateral in a practice known as back leverage. JPMorgan's action was preemptive, driven by changes in the bank's valuations rather than actual loan losses or defaults. Additionally, no margin calls were triggered. A margin call occurs when a lender determines that the value of a borrower's collateral has fallen below a required threshold, demanding the borrower either post additional collateral or repay part of the loan immediately.

JPMorgan was also able to act without having to wait for covenants to trigger. Covenant triggers are specific contractual conditions, such as missed payments or a fund's net asset value falling below a set level, that must be met before a lender can formally reduce a borrowing facility or demand repayment. Most banks require such triggers to ensure they have increased rights when the conditions are met. Lenders also benefit from known and stable collateral values when they remain compliant. But in this case, JPMorgan had reportedly reserved the contractual right to revalue private credit assets at any time.

Even without defaults, margin calls, or covenant triggers, private credit funds could face significant pressure if other major lenders follow JPMorgan's lead. Private credit would then be at risk of a dual squeeze: investor outflows and reduced borrowing capacity simultaneously. That said, the redemption caps discussed above serve as a structural protection against outsized outflows, preventing funds from being forced into distressed asset sales. Meanwhile, funds continued to attract new subscriptions in Q1 2026 ($2B for BCRED, $840M for HLEND) even as retail redemptions have risen, suggesting some stability.

Whether the pressure intensifies depends on if credit fundamentals deteriorate, or if this is a liquidity story driven by narrative rather than losses. The underlying credit data shows more stability than the redemptions suggest. Private credit default rates stood at 2.46% in Q4 2025, per Proskauer's Private Credit Default Index. This is within historical norms and nowhere near the 10%+ levels seen during the GFC. Direct lending spreads have also remained stable at 500–700 basis points over SOFR since 2023, with no signs of the widening that signals systemic stress.

Private Equity

Software has represented roughly 25% of private equity deal value over the past five years, making it one of the sector's defining exposures. The vulnerability is concentrated in specific vintages, as sponsors who deployed capital aggressively in 2021–2022 did so at premium multiples. For private software company M&A transactions, EV/Revenue peaked at 6.7x and EV/EBITDA at 39.9x during that period. By H2 2025, those metrics compressed to 3.1x and 26.1x respectively.

Those 2021–2022 portfolios now face pressure from public market comparables deteriorating, which resets exit benchmarks. As the market increasingly questions whether certain software business models remain defensible in an AI-driven environment, IPO paths will likely be restricted and monetization timelines are likely to extend further.

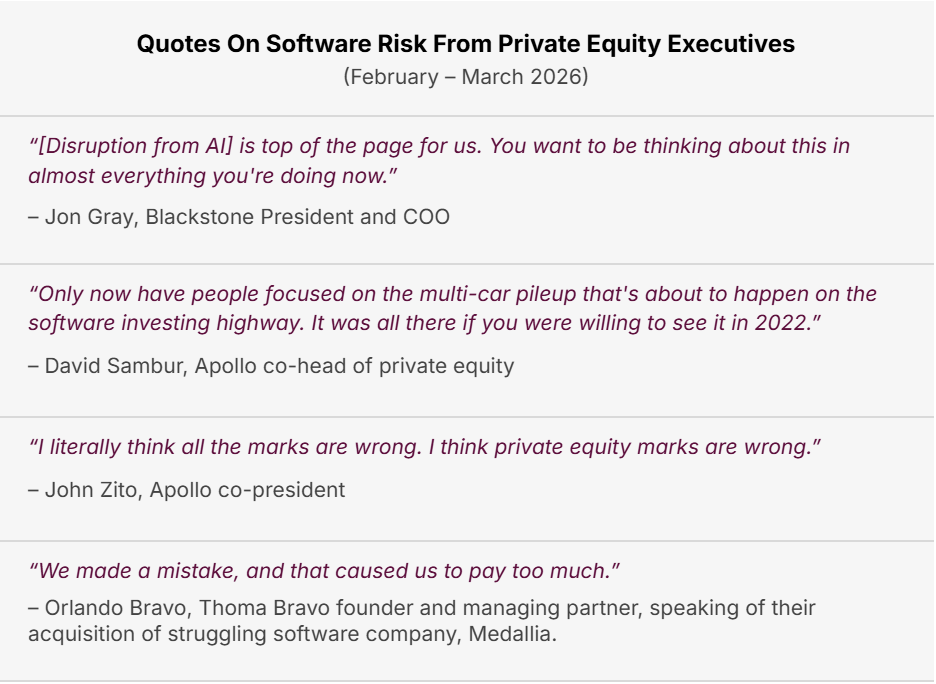

The implications are emerging slowly, visible primarily through candid executive commentary. John Zito, co-president of Apollo, outlined his concerns that software companies bought by private equity at high multiples and funded by cheap debt are particularly exposed.

Software Fundamentals: What the Data Shows

Bearish Case

Revenue Growth Is Compressing

According to Bain & Company, median revenue growth for public SaaS companies has fallen from 27% in 2021 down to 10% in 2025. While the 2021 peak was partly driven by pandemic-era digitization spending, the decline has continued well past reasonable normalization. The SEG SaaS Index reports median trailing twelve months revenue growth at approximately 12.9%, consistent with Bain’s data and a useful cross-check given they use different methodologies.

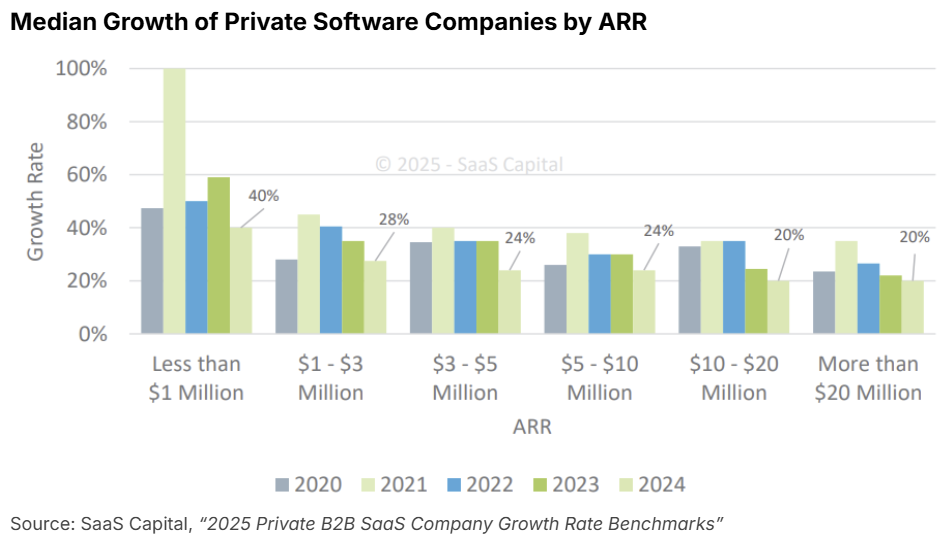

The same trend is visible in private markets. SaaS Capital's 2025 survey of 1,000+ private SaaS companies shows median growth declining steadily across every revenue band from $1M–$20M+.

KeyBanc Capital Markets and Sapphire Ventures' joint SaaS survey shows an even steeper revenue growth decline among private companies that average slightly larger than those in the SaaS Capital study. Among surveyed companies with a median annual recurring revenue (ARR) of $26M, ARR growth fell from 31% in 2022 to 15% by 2024.

Some growth deceleration is expected and normal as software companies mature and markets saturate. What makes the current period notable is that the deceleration is happening simultaneously across multiple metrics: revenue growth, net revenue retention, and Rule of 40. All three declines happening at the same time, alongside AI emerging as a legitimate competitive threat, is hard to dismiss.

Net Revenue Retention Under Pressure

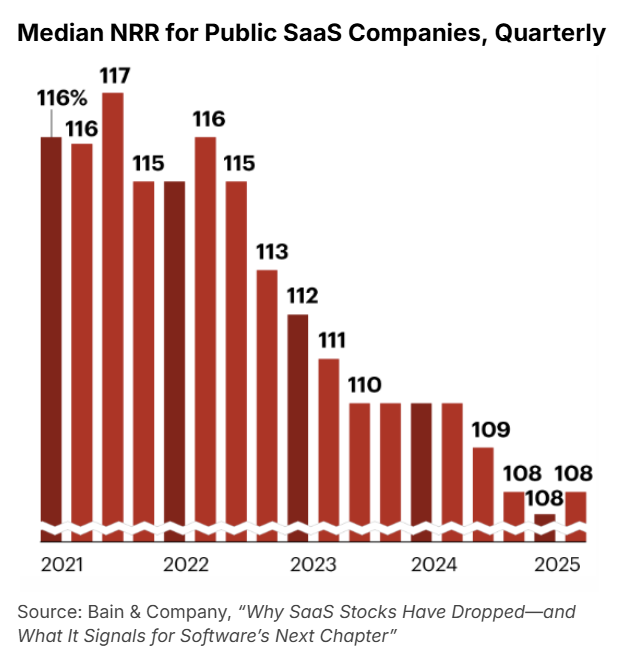

Net revenue retention (NRR), the percentage of revenue retained and grown from existing customers year-over-year, is one of the most important metrics for a SaaS business. An NRR above 100% means the business grows even without acquiring a single new customer. Bain shows median NRR for public SaaS companies has declined steadily from 117% in early 2021 to 108% by 2025 (see the chart below).

Bain notes that penetration curves are flattening for core functionality and seat growth is becoming a less meaningful expansion driver. For example, rather than purchasing 500 seats, an enterprise might buy 450 and deploy an AI agent for the rest. Bain estimates AI could automate between 30% and 50% of activity across key enterprise functions, pointing to meaningful seat compression and further NRR pressure ahead.

The current median NRR of the SEG SaaS Index at the time of this publication is 106%, a further step down from the Bain figure and below the 110%+ levels that investors historically associated with SaaS performance. Among private companies, KeyBanc's data shows the same directional story: median net dollar retention declined from 106% in 2022 to 101% by 2024.

Rule of 40 Is Harder to Reach

The Rule of 40 holds that a company's revenue growth rate plus its free cash flow margin should sum to at least 40%, balancing growth against profitability. This benchmark has always been aspirational. McKinsey analyzed more than 200 software companies between 2011 and 2021 and found that only one third of companies achieve 40% and even fewer maintain it.

SEG reports a median Rule of 40 score of 27.0% across its 120+ public constituents, and only 24.5% of companies clear the 40 threshold today. To be fair, a score above 25% reflects a growing and profitable business, just not one at the pace and efficiency the benchmark demands.

Bullish Counterpoint: Underlying Businesses Are Stronger Than the Selloff Implies

In the Q4 2025 earnings season, 93% of S&P 500 software companies beat profit estimates compared with 74% for the broader index. The category is delivering results, yet valuations reflect a level of distress the fundamentals don't currently support.

In mid-March 2026, Deutsche Bank upgraded its outlook on software within the tech sector. Strategists noted that after consulting with industry experts and AI models they have “not come across a single software company that expects a negative revenue effect from AI in 2026.”

Profitability Has Improved Dramatically Across Public SaaS

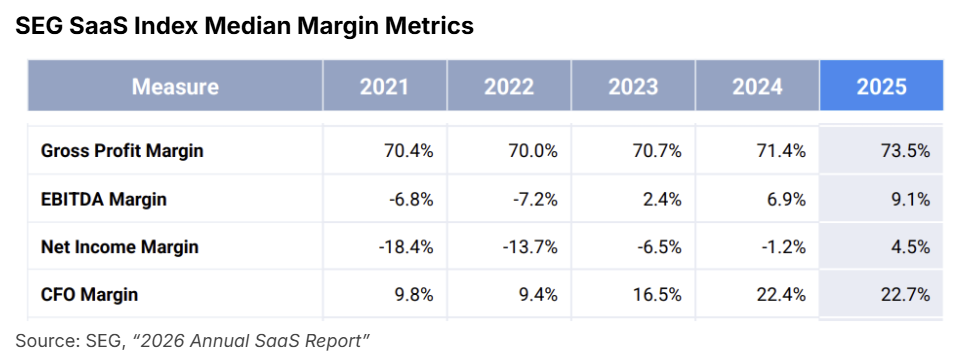

SEG's 2026 Annual SaaS Report documents a profitability transformation that has received less attention than the revenue slowdown narrative. Median EBITDA margin of public SaaS companies improved steadily from negative in 2022 to positive 9.1% by 2025. At the same time, median net income margin turned positive in 2025 after being in the red for four straight years. Median CFO margin, or cash flow from operations as a percentage of revenue, nearly tripled from 2022 to 2025.

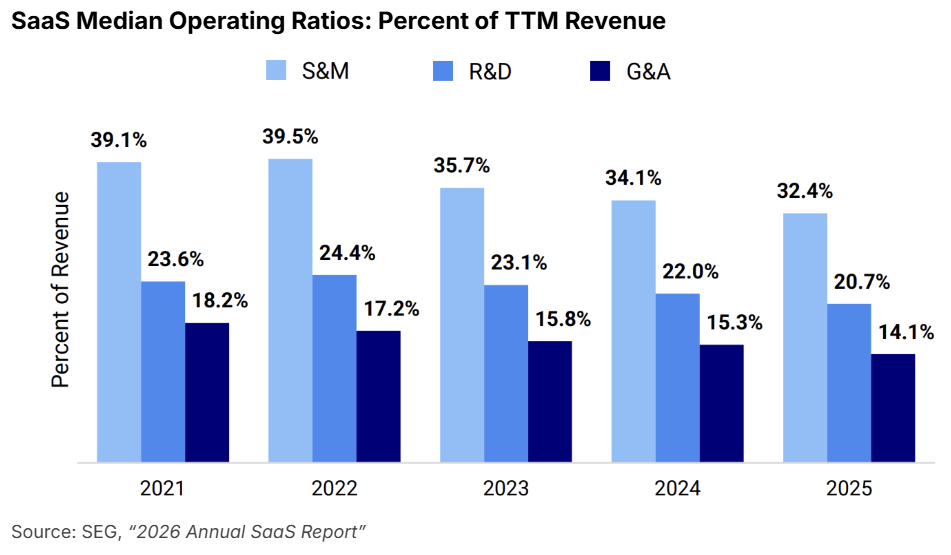

Cost Discipline Across Every Spend Category

The same SEG report shows what is driving the margin improvement in SaaS. Every major cost line as a share of revenue—median sales and marketing (S&M) spend, research and development (R&D) spend, and general and administration (G&A) expenses—all declined from 2022 through 2025.

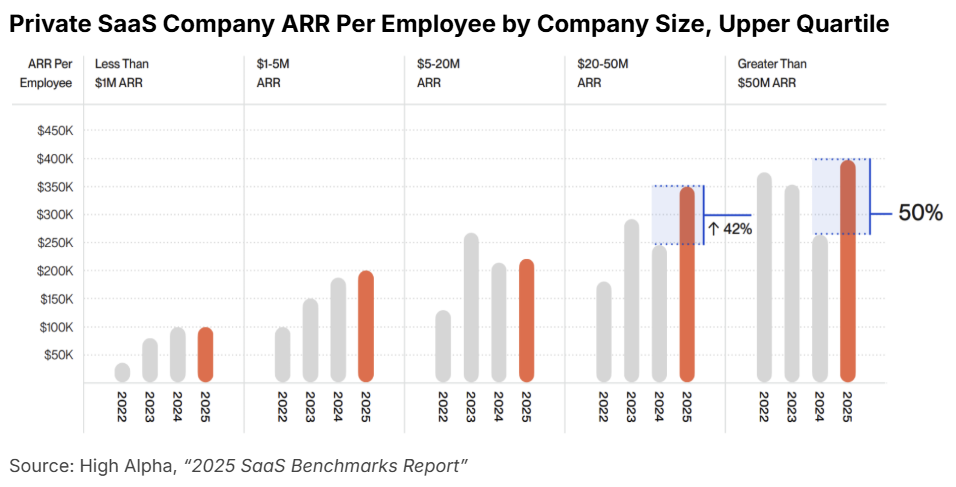

Efficiency Gains Are Compounding At Scale

ARR per employee is an emerging productivity benchmark, in part because it moves alongside efficiencies gained from AI adoption. According to High Alpha, median ARR per employee at public SaaS companies increased more than 10% year-over-year in 2025. The pattern is equally visible in private markets. Among private companies with $20–50M in ARR, the upper quartile median ARR per employee grew 42% year-over-year. The growth was even more pronounced for companies with over $50M in ARR (50% YoY), reflecting the fundamental shifts in how software businesses are being run: leaner teams combined with AI-assisted workflows.

Implications for Investors

The data presented above reflects where software businesses stand today, but the SaaSpocalypse thesis is a forward-looking argument about what AI will do to these businesses over the coming years. The question is not whether fundamentals are sound now, but whether they will remain so. Three implications stand out for investors navigating this in real time:

1) A Broad Selloff Does Not Mean Broad Risk

For investors with exposure to public software stocks, the selloff and slowing revenue growth can look like a category-wide verdict. Yet several SaaS subsectors have held up well over the last year. Revenue multiples for the analytics & data management subsector expanded in 2025, from 3.4x to 4.5x. Meanwhile, subsectors including DevOps & IT, ERP & supply chain, and security continue to command high multiples. These products are deeply embedded in core enterprise workflows, carry high switching costs, and play a foundational role in enabling AI, automation, and operational resilience.

2) Private Credit Stress Is Real But Not Yet Fundamental

While redemption pressures across private credit funds are real, the enforced caps are not signs of systemic vulnerability. The caps exist precisely to prevent forced selling of illiquid assets during periods of investor anxiety, and the underlying credit data does not currently support a crisis narrative: default rates remain within historical norms, spreads have held steady, and underwriting standards have not materially deteriorated.

That said, specific developments warrant close attention. JPMorgan's decision to mark down software loan collateral is meaningful because of what happens if other major lenders follow: a simultaneous squeeze of investor outflows and reduced borrowing capacity. Watch default rates, spread movements, and lender behavior as the leading indicators that separate a sentiment-driven episode from a fundamental one.

3) Whether Software Competes With or Harnesses AI Is What Matters

As the WSJ reported in late March 2026, several Fortune 500 technology executives indicated they are currently using AI to build small apps and customizations rather than replacing existing vendors, suggesting the displacement scenario, while plausible, is not yet playing out at scale.

The useful distinction for investors is not software versus AI broadly, but which software companies compete with AI and which ones enable or embed it. Companies with high switching costs, proprietary data, and deep integration into core enterprise workflows are structurally better positioned than those offering narrow and replicable functionality. The metrics covered in this paper are the right instruments to track that distinction over time: NRR, Rule of 40, margins, and ARR per employee.

Download the white paperfor the full list of citations.

Long Angle members can reach out to the Long Angle Investments team with any questions on software and AI investments, and opportunities to invest. Non-members can learn more about Long Angle at longangle.com and apply for membership here.

Ready to connect with like-minded peers navigating similar wealth decisions?

Join Long Angle, a private community where successful entrepreneurs, executives, and professionals collaborate on wealth strategies, investment opportunities, and life's next chapter.