What is a Schedule K-1? Private Markets Tax Guide

The Private Markets Tax Guide covers the key tax concepts and administrative considerations that arise most frequently for private market investors. These include Schedule K-1s and pass-through taxation, filing timelines and extensions, state filing requirements, tax treatment by asset class, CPA costs, and strategies for reducing the tax burden. Note that this is for informational purposes only and is not tax advice.

Access the Full Investment Guide Here

What is a Schedule K-1?

What is a K-1?

A Schedule K-1 is an annual tax form issued to each investor in a partnership. Rather than the fund paying taxes itself, it passes its income, losses, and deductions to investors, who each report their share on their personal tax return. This is called pass-through taxation. Unlike a 1099, which reports income from stocks, bonds, and bank interest, a K-1 is more complex because it reflects your share of all the underlying activity of a partnership.

Why does it exist?

Most private funds are structured as limited partnerships. Partnerships don't pay entity-level taxes, and the tax obligation rests with the individual partners.

How it works at Long Angle?

When you invest through a Long Angle Special Purpose Vehicle (SPV), there are two K-1s:

The underlying fund sends a K-1 to the Long Angle SPV.

Long Angle then prepares and sends a pass-through K-1 to each member investor.

This two-step process adds 1-3 weeks to the timeline. Since many underlying funds deliver K-1s after the April 15th deadline, you will almost always need to file a federal tax extension in years you hold private investments. This is normal, expected, and free to file.

Filing an extension

The extended deadline for individuals is October 15th. Many CPAs actually welcome filing an extension, as it moves your return outside the April rush and gives everyone more time for a careful, accurate return. The extension does not extend the deadline to pay estimated taxes, however, which is still April 15th. When you file in October, your CPA reconciles your earlier estimate against your actual liability. Most receive a refund or owe a minor balance.

How Many K-1s and When?

How many should you expect?

This depends entirely on how many private market investments you hold. A member with five Long Angle investments might receive five K-1s, one per investment. Some funds hold assets in multiple states or have complex structures, meaning a single fund investment can generate several K-1 documents.

Long Angle members who are active investors across multiple asset classes sometimes manage 10 to 20 K-1s per year. With some organization and the right CPA, this is manageable.

When do they arrive?

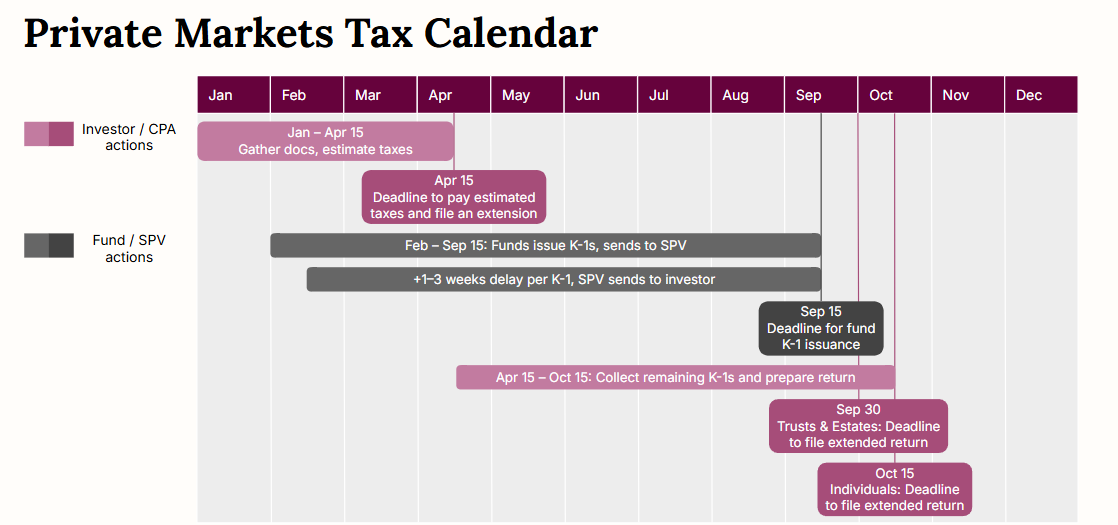

Most private market funds request a filing extension, pushing their K-1 issuance deadline to September 15. In practice, K-1s can arrive any time between February and September depending on the fund (see a calendar illustration below).

The extension is your friend

Most private market investors file a federal tax extension. A federal extension is free and gives you until October 15 to file your personal return.

What to do in the meantime

Store every K-1 in a dedicated folder as they arrive and coordinate with your CPA on timing for when to send them over. A simple spreadsheet tracking which investments have and haven't sent K-1s yet helps avoid missing anything. Amended K-1s are common, so funds might send corrections after the original. CPAs should be aware that K-1s can be revised.

For illustrative purposes only

How Private Investments Get Taxed

Public vs. private market tax treatment

Private market investments are not inherently taxed at higher rates than public market investments. The tax treatment depends on the type of income, not the vehicle. For most investors, the government's cut is comparable to what you would pay on similar public market income. In some cases, private markets actually compare favorably.

Private equity and venture capital

PE and VC exits are often taxed as long term capital gains when underlying assets have been held for over a year, just like a public stock. These gains are taxed at lower rates than ordinary income.

Real estate

Real estate income from private funds typically produces a mix of ordinary income from rents and capital gains from property sales. RE funds often use depreciation deduction strategies that shelter income and reduce your effective tax rate in the short term.

Private credit

Private credit is typically considered interest income, and is taxed as ordinary income at your marginal rate. This is the same treatment as bond interest or a savings account.

Complexity caveat

A mix of strategies in the same year can produce capital gains, ordinary income, and deductions that make tax planning complex (see below). This is where a good CPA earns their fee.

CPA Costs

What drives accounting costs

Number of K-1s.

Number of state filings.

Complexity of income types: capital gains vs. ordinary income vs. depreciation.

Whether your CPA has experience with private market K-1s: inexperienced CPAs take longer and may charge more.

What to watch out for

CPAs vary widely in how they charge for K-1 complexity. Some include K-1s in a flat annual fee; others charge per form or per state filing. Make sure you understand your CPA's fee structure before your K-1 volume grows.

Questions to ask your CPA

Do you have experience with private market K-1s?

Do you routinely file extensions for clients with private market investments?

Are you comfortable filing in September or October? (Some inexperienced CPAs will apply earlier internal deadlines that don’t account for late-arriving K-1s.)

How do you charge for additional K-1s: per form or as part of a flat fee?

Will additional state K-1s result in additional charges?

Cost Benchmarks

Long Angle members report a median annual CPA cost of $3,000, though costs vary significantly based on the number of K-1s and state filings.

The Juice vs. the Squeeze

At what point does private market investment complexity justify the return? There is no universal answer, but here is a practical framework.

Size your investments accordingly

Taxes and accounting fees are a drag on net returns. The smaller the investment, the larger that drag as a percentage of your gains. A $10,000 investment generating $500 in incremental accounting fees is a 5% drag before any returns. A $500,000 investment with the same $500 cost is a 0.1% drag.

Small allocations across numerous investments may not justify the administrative overhead. Concentrate enough in each investment that the return potential clearly outweighs the cost. The right minimum varies by personal situation and tax profile, but the math should work clearly in your favor before committing.

Set up the right infrastructure

The first K-1 and filing an extension can feel unfamiliar. But each additional K-1 adds relatively little incremental burden once the infrastructure is in place. This is especially true if you have the right CPA. As one Long Angle member put it, “it’s only a pain if you try to do it yourself.”

Members who have been through it typically agree that once you accept October 15th as your real tax deadline (not April 15th) and set up a process for it, it becomes routine.

State Filings: What to Expect

How state filings are triggered

A state K-1 is generated when a fund has income sourced from assets or activity located in that state. For example, a real estate fund with properties in California and Texas would generate a state K-1 for California but not Texas, since Texas has no state income tax.

Not every K-1 requires a state return

Most states have de minimis thresholds: minimum income levels below which no filing is required. If your share of income from a particular state is very small, which is common in diversified funds, no state return is needed.

What Long Angle members actually experience

Members with diversified PE and credit portfolios typically file in only one or two additional states per year. Real estate is the main exception. Funds with properties across multiple states can generate multiple state filing requirements, particularly in high-tax states like California, New York, and Massachusetts.

Why composite filings are usually the wrong choice

Some states allow a fund to file a single composite return on behalf of all non-resident partners. This sounds like a convenience, but it comes with real drawbacks: composite returns are taxed at the highest marginal state rate, you lose the ability to carry forward losses into future years, many states restrict deductions and credits, and your state of residence cannot be removed. Discuss with your CPA whether to opt in or out before the deadline.

Tax Complexity by Strategy

| Strategy / Asset Class | Form Type | State Filing Likelihood | Complexity Level |

|---|---|---|---|

| Evergreen Funds | Simplified K-1 or in some cases a 1099 | Low | Lowest: fewer line items and lower administrative burden than other private fund investments. If a fund issues a 1099, it will be converted to a K-1 for SPV investors. |

| Private Equity | Federal K-1 | Low | Low: income is typically a mix of capital gains and ordinary income, which can vary significantly year to year depending on fund activity and exits. |

| Venture Capital | Federal K-1 | Low | Low: K-1s often show little activity for years, followed by a larger gain when a portfolio company exits or goes public. |

| Private Credit | Federal K-1 | Low | Low: income is predominantly ordinary interest income, taxed at higher rates than capital gains but consistent and straightforward to report. |

| Real Estate | Federal K-1 + State K-1s | High: properties in multiple states generate state-level K-1s wherever the fund has income. | Moderate: real estate funds frequently use accelerated depreciation strategies (cost segregation) to front-load tax deductions, which trigger additional state filings. |

| Energy | Federal K-1 + State K-1s | Moderate: state filings may be required in producing states. | High: oil and gas can generate tax deductions like Intangible Drilling Costs (IDCs) and depletion allowances (deduction on the extraction of natural resources). Renewable energy may generate Investment Tax Credits (ITCs). These are highly valuable but require careful handling from your CPA. |

International Investors

FDAP vs. ECI

US-source income paid to foreign investors generally falls into one of two categories. Fixed, Determinable, Annual, or Periodic (FDAP) income, such as dividends and interest, is subject to US withholding tax. This tax is withheld and paid by the fund before distributions reach the investor, satisfying the US tax obligation without requiring a personal filing.

Effectively Connected Income (ECI), income connected to a US trade or business, is taxed at US rates and requires the investor to file a US tax return. Some US private fund investments are classified this way and generate ECI for non-US investors. When ECI is expected, Long Angle flags it in the offering materials.

Some funds offer a blocker fund structure that eliminates the US filing requirement for ECI by establishing a US C-corporation. The investor receives dividends from the corporation, which are treated as FDAP income and subject only to withholding tax.

Withholding taxes

US partnerships are required to withhold taxes on behalf of foreign partners before distributions reach the investor, which can create cash flow timing issues. US tax treaties may reduce applicable withholding rates depending on the country.

FIRPTA

The Foreign Investment in Real Property Tax Act (FIRPTA) applies to foreign investors in US real estate. Gains from the sale of US real property interests are subject to US tax and withholding, regardless of where the investor is located.

Home country reporting

Investing in a US fund may trigger reporting obligations in your home country and create timing mismatches even when US withholding is handled. Consult a cross-border tax advisor before investing.

Reducing the Tax Burden

Evergreen funds

Evergreen funds typically produce a 1099 or simplified K-1 rather than the complex multi-state K-1s of traditional drawdown funds. Underlying Long Angle investments that produce a 1099 will still be converted to a K-1 because of the SPV structure, but the K-1 will be simplified to reflect only the relevant fields from the 1099.

Self-Directed IRA (SDIRA) or Roth IRA

Investing through an individual retirement account means K-1 income is tax-deferred (traditional IRA) or tax-free (Roth IRA). K-1s go to your custodian instead of you personally, and distributions are paid back into your SDIRA, eliminating them from your personal tax return entirely. Note that UBTI is an exception (see below).

IRA exceptions

Retirement account holders should be aware of Unrelated Business Taxable Income (UBTI). Certain private fund strategies can generate UBTI, which creates a tax liability even inside a retirement account. UBTI requires additional filing and the resulting tax drag reduces your net return. Check whether a fund is expected to generate UBTI before investing through an IRA. Long Angle's investment memos flag this if relevant. Some funds offer a UBTI blocker structure, which uses a C-corporation to prevent UBTI from flowing into your retirement account.

Many large custodians like Fidelity and Schwab are not designed to support third-party private investments. Requirements such as multiple years of audited financials, along with slow processing times, can create significant barriers for investing in private funds. Most members with this setup use AltoIRA or other partnered custodians.

Where to Go From Here

Long Angle Investments

Long Angle members can reach out to the Long Angle Investments team with any questions about what to expect administratively for any offering.

For specific tax advice, please consult your CPA or tax professional. We are not tax advisors and this guide is not a substitute for personalized guidance.

Investment Memo Transparency

Long Angle's investment memos include a Tax Reporting and Treatment section for every offering, noting expected K-1 timing, if state K-1s are anticipated, and whether UBTI or ECI is expected.

This information is available before you commit.

Long Angle Member Community

Long Angle members are actively discussing tax strategies, CPA recommendations, and K-1 administrative best practices.

Non-members can learn more about Long Angle at longangle.com and apply for membership here.

Every member's tax situation is unique. Treat peer advice as a starting point, not a substitute for your own CPA or tax professional.

Further Reading

The IRS Partner's Instructions for Schedule K-1 provides an introduction to K-1s and key definitions. The instructions also include a full breakdown of what each box on your K-1 means and how to report it on your return, which is most useful once you have your first K-1 in hand.

Read Long Angle’s two Private Markets Terminology Guides:

See our Private Markets Glossary for a searchable list of private markets terms and definitions.

Ready to connect with like-minded peers navigating similar wealth decisions?

Join Long Angle, a private community where successful entrepreneurs, executives, and professionals collaborate on wealth strategies, investment opportunities, and life's next chapter.