Private Markets Terminology: Asset Classes & Strategies

The Private Markets Terminology Guide is an introduction for investors newer to private markets. It covers asset classes, return metrics, parties involved, structures, fees, the investment lifecycle and more.

Access the Full Investment Guide Here

Table of Contents

Private Equity: Strategy Concepts (buyout, LBO, growth equity), Valuation & Value Creation (EBITDA, Enterprise Value, Equity Value), Equity Lifecycle

Private Credit: Structure & Strategies (capital stack, direct lending, mezzanine), Strategies & Vehicles (BDCs, CLOs, ABF), Loan Terms (spread, covenant, FCCR, PIK)

Real Estate: Fundamentals (NOI, cap rate, LTV), Strategies & Asset Types (core, core-plus, value-add, opportunistic, multifamily, industrial, retail)

Secondaries: LP-led, GP-led / Continuation Vehicle, NAV Discount

Why This Guide Exists

Private markets have their own vocabulary

If you've ever opened an investment memo and felt like you were reading a foreign language, you're not alone and you're not behind. This guide is designed for investors newer to private markets to use as an educational resource and return to as a quick reference guide when evaluating opportunities. Understanding key terms is the first step in diligence.

The following covers asset classes and strategy terms. For more, see our companion guide: Private Markets Terminology: Return Metrics & Investment Concepts.

Asset Classes: Terms to Know

Private Equity (PE)

Ownership stakes in privately held companies that are not traded on public stock exchanges. GPs acquire stakes in businesses with the goal of growing their value and exiting at a profit. Strategies range from acquiring mature companies to investing in earlier-stage, faster-growing businesses. Value creation in private equity typically comes from three levers: earnings growth, multiple expansion, and debt paydown, all of which are covered below.

Sub-asset classes include GP Stakes (minority ownership in fund managers themselves, providing exposure to their fees and carried interest), Search Funds (capital raised by an entrepreneur to find, acquire, and operate a single company), and Venture Capital (see definition below).

Venture Capital (VC)

A subset of private equity focused on early-stage (startups) and growth-stage companies with high potential but are often not yet profitable. Returns are driven by a small number of outsized winners. Loss rates are higher than PE, but top performers can return many multiples of invested capital.

Private Credit (PC)

Non-bank lending to companies, also referred to as private debt. A private credit fund pools investor capital to make a portfolio of loans backed by company cash flows or assets. The fund manager underwrites and monitors the loans, earning returns through interest income and fees. Private credit sits lower on the risk spectrum than equity but higher than investment-grade public bonds.

Real Estate (RE)

Ownership stakes in physical properties including office, industrial, residential, retail, hospitality, and self-storage, accessed through direct ownership, funds, or real estate investment trusts (REITs). Returns come from rental income and property appreciation. Strategies range from stable core holdings to value-add repositioning and ground-up development.

Alternatives

A broad catch-all for strategies outside traditional public stocks and bonds. While PE, PC, and RE are sometimes categorized as alternatives, Long Angle treats them as distinct asset classes. Here, alternatives refers to more specialized strategies including hedge funds, precious metals, collectibles, crypto, natural resources, litigation finance, and royalties. These are often characterized by low correlation to public markets.

Real Assets

Physical or tangible assets including real estate, natural resources, commodities, infrastructure, timberland, and farmland. Preferred for their tendency to hold up through inflation, generate income, and move independently of public markets.

Infrastructure

Assets that provide essential services to people and economies: power generation and transmission, transportation, water, communications, digital infrastructure such as data centers and fiber networks, and social facilities like hospitals. Infrastructure investments typically generate stable, long-term contracted or regulated cash flows, making them relatively resilient through economic cycles.

Energy

Investments in the exploration, production, transportation, and storage of energy commodities including oil, gas, and renewables. Returns are influenced by commodity prices, production volumes, and whether assets are still in development or producing. Can offer meaningful tax advantages and low correlation to public markets.

Private Equity: Strategy Concepts

Buyout

Majority ownership in mature companies, where the GP restructures finances, governance, operations or some combination to maximize returns. The most common PE strategy. Valued on EBITDA multiples.

Leveraged Buyout (LBO)

A buyout where the GP uses a combination of investor equity and debt to acquire a company. The debt is typically secured against the acquired company's assets and cash flows, and repaid over the holding period. Leverage amplifies both returns and risk.

Growth Equity

Minority ownership in companies that are more mature than a startup, but less established and faster-growing than a typical buyout target. These companies need capital to grow, commercialize, or professionalize their operations.

Add-on Acquisition (Bolt-on)

The purchase of a smaller company to merge into an existing portfolio company, also called a bolt-on. Add-ons allow the GP to grow a portfolio company through acquisition rather than organic growth alone. Once merged as a combined entity, the add-on company’s earnings may be immediately valued at a higher multiple, called multiple arbitrage. Roll-up strategies are a common application, where a GP systematically acquires many smaller companies in an industry.

Top/Bottom Quartile & Performance Persistence

Manager returns are typically benchmarked against peers. Top quartile managers are the top 25% of performers; bottom quartile the lowest 25%. Private equity has historically shown performance persistence: top quartile managers tend to remain top quartile across successive funds.

Private Equity: Valuation & Value Creation

EBITDA

Earnings Before Interest, Taxes, Depreciation and Amortization. The primary profitability metric used to value PE portfolio companies.

Enterprise Value (EV) and Equity Value

Enterprise Value (EV) is the total value of a business, representing what it would cost to acquire the company outright including both equity (ownership stakes) and debt. EV is typically derived from an EBITDA multiple: the ratio expressing how many times EBITDA a buyer is willing to pay. In private equity, companies are typically bought and sold based on Enterprise Value. There are three primary value creation levers: earnings (EBITDA) growth, multiple expansion, and debt paydown (see below).

Equity Value is what remains for equity holders after subtracting net debt (total debt minus cash on hand) from Enterprise Value.

Equity Value = EV - Net Debt

As a result, upward and downward changes to EV and net debt flow directly to equity holders.

Multiple Expansion

The increase in valuation multiple between when a company is bought and when it is sold. If a GP buys a company at 8x EBITDA and sells it at 12x EBITDA, the difference is pure multiple expansion even if the company's earnings didn't grow.

Debt Paydown

When a company uses its operating cash flows to pay down the debt used to acquire it, the equity value increases dollar for dollar (since equity value is EV minus net debt). Even if the company's enterprise value stays flat, reducing debt directly increases what equity holders own.

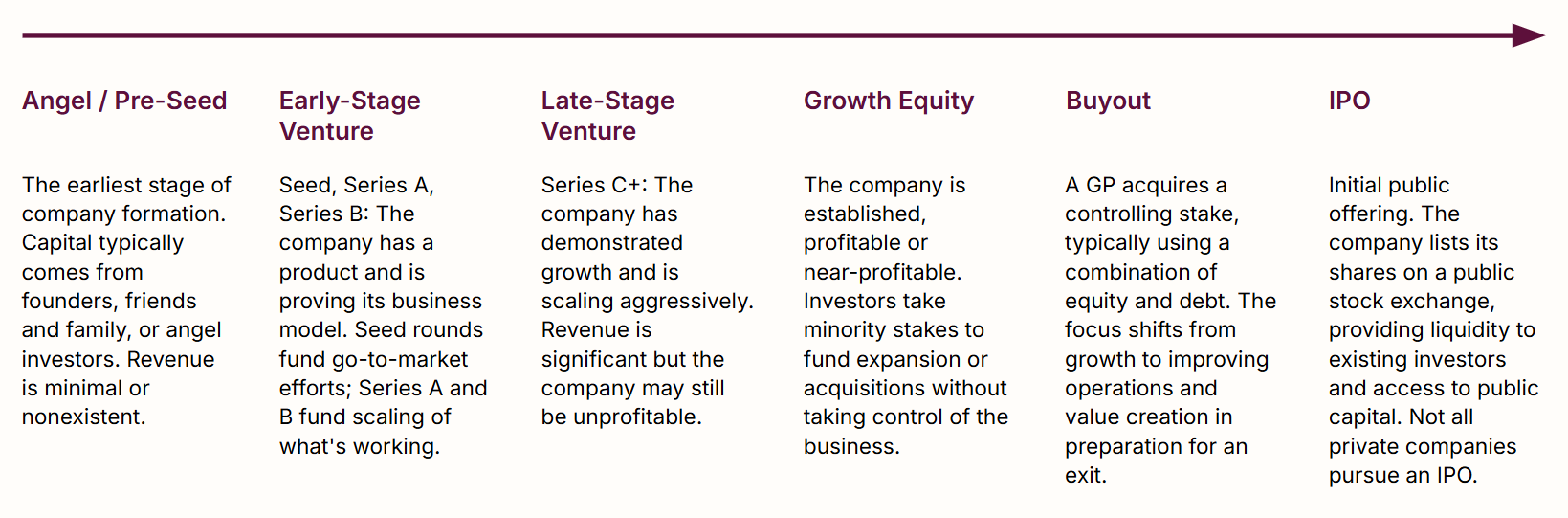

Equity Lifecycle

Illustrative example of a private equity drawdown fund

Timeline is for illustrative purposes only. Not all companies experience each stage, and the boundaries between stages are not always clearly defined. Most companies are acquired, merge, or remain private without ever reaching IPO.

Angel / Pre-Seed

The earliest stage of company formation. Capital typically comes from founders, friends and family, or angel investors. Revenue is minimal or nonexistent.

Early-Stage Venture

Seed, Series A, Series B: The company has a product and is proving its business model. Seed rounds fund go-to-market efforts; Series A and B fund scaling of what's working.

Late-Stage Venture

Series C+: The company has demonstrated growth and is scaling aggressively. Revenue is significant but the company may still be unprofitable.

Growth Equity

The company is established, profitable or near-profitable. Investors take minority stakes to fund expansion or acquisitions without taking control of the business.

Buyout

A GP acquires a controlling stake, typically using a combination of equity and debt. The focus shifts from growth to improving operations and value creation in preparation for an exit.

IPO

Initial public offering. The company lists its shares on a public stock exchange, providing liquidity to existing investors and access to public capital. Not all private companies pursue an IPO.

Private Credit: Structure & Strategies

See our Private Credit Investment Guide.

The Capital Stack

Private investments are structured in priority order for repayment in the event of default or liquidation:

Senior Debt: paid first, lowest risk/return

Mezzanine Debt: higher risk, higher return

Preferred Equity: paid after all debt

Common Equity: paid last, highest risk/potential return

First Lien

The most senior debt position in the capital stack. Because of their priority for repayment, first lien loans carry the lowest risk and lowest return among credit strategies.

Direct Lending

Non-bank lending directly to middle-market companies. Typically first lien and secured (backed by the company's assets). Loans are typically floating rate, meaning the interest rate adjusts with market rates to protect lenders against interest rate movements.

Mezzanine

Debt that sits between senior debt and equity in the capital stack, junior to first lien lenders but senior to equity holders. The term "mezzanine" reflects its middle position in the structure. Also referred to as subordinated or junior debt, mezzanine is typically unsecured or lightly secured and carries higher interest rates than senior loans to compensate for the additional risk.

Opportunistic Credit

A strategy targeting higher-risk, higher-return credit opportunities. This includes distressed debt (lending to companies in financial stress or acquiring their existing debt at a discount) and special situations (complex transactions requiring creative structuring). Opportunistic credit targets equity-like returns with some downside protection through the debt structure.

Private Credit: Strategies & Vehicles

Business Development Company (BDC)

A regulated investment vehicle providing investors exposure to diversified private credit portfolios. Non-traded BDCs offer periodic liquidity valued at net asset value (NAV): the fund’s total asset value minus liabilities. Public BDCs trade on major stock exchanges and offer daily liquidity and real-time, market-driven pricing.

Collateralized Loan Obligation (CLO)

A vehicle that pools a diversified portfolio of corporate loans and issues multiple tranches of securities to investors, each with a different risk and return profile. Senior tranches are paid first and carry the lowest risk and yield. Mezzanine tranches offer higher yields in exchange for more risk. Equity tranches absorb losses first but receive all residual cash flows, offering the highest potential yield.

Asset-Based Finance (ABF)

Lending secured by specific assets rather than a borrower's overall cash flows, typically across large, diversified pools. Common asset types include receivables, inventory, equipment, real estate, and infrastructure. Specialty finance is a subset covering specific financial assets or cash flows, including consumer loans, auto loans, and equipment leases. The underlying pool could include thousands of loans across different borrowers and geographies.

Broadly Syndicated Loans (BSL)

Large-scale corporate loans originated by a bank and then sold (syndicated) to a broad group of institutional investors. This is considered a public credit strategy, also referred to as syndicated loans or leveraged loans. BSLs are highly liquid and trade in a secondary market. Like private credit, they are typically floating-rate but generally have looser lender protections.

Private Credit: Loan Terms

Spread

The interest rate premium a borrower pays above a benchmark rate. The most common benchmark is SOFR (Secured Overnight Financing Rate). A loan quoted as "S+200" means SOFR plus 200 basis points (2%). Wider spread means more risk and reward for the lender.

Covenant

A condition in a loan agreement that the borrower must maintain (e.g., minimum EBITDA levels) that protects lenders. Private credit typically has stronger covenants than public credit markets.

Fixed Charge Coverage Ratio (FCCR)

A measure of a borrower's ability to meet its fixed financial obligations (e.g., debt service, lease payments, recurring costs). Lenders use FCCR as a covenant to ensure borrowers maintain sufficient cash flow. A ratio above 1.0x means there’s enough income to cover obligations.

Original Issue Discount (OID)

When a loan is issued at a price below its face value. For example, a $100 loan issued at $98 gives the lender a $2 gain at repayment, representing additional yield on top of the interest rate.

Payment-in-Kind (PIK)

Interest that is not paid in cash but instead added to the outstanding loan balance. PIK allows borrowers to preserve cash in the near term but increases the total debt burden over time. Common in leveraged buyouts where near-term cash flow is limited. PIK is characterized as “good” or “bad”. Good PIK is structured at origination, giving the borrower the option to defer interest and preserve cash for growth. Bad PIK is triggered mid-loan because the borrower cannot make cash interest payments.

Warrant

A right granted to a lender to purchase equity in the borrower at a predetermined price. Warrants allow lenders to participate in the upside of a company's growth alongside their debt return.

Real Estate: Fundamentals

Net Operating Income (NOI)

Revenue from a property minus operating expenses, before debt service and taxes. The core profitability metric for real estate and the equivalent of EBITDA in private equity.

Capitalization Rate (Cap Rate)

NOI divided by property value. Used to compare the yield of different real estate investments. Lower cap rate equals higher valuation. Note: cap rate is the inverse of a PE multiple. A 5% cap rate is equivalent to a 20x earnings multiple.

Loan to value (LTV)

The ratio of debt to the property's appraised value. Higher LTV means more leverage, more risk. For example, a property valued at $2M with $500K in outstanding debt has an LTV of 25%.

Debt Service Coverage Ratio (DSCR)

A measure of a property's ability to cover its debt payments from operating income. Calculated as NOI divided by total debt service (principal and interest payments). A DSCR above 1.0x means the property generates enough income to cover its debt obligations. Lenders typically require a minimum DSCR as a condition of financing.

Occupancy

The percentage of a property's rentable space that is currently leased and generating income. Higher occupancy drives higher NOI and therefore higher property value. Occupancy is a key indicator of asset quality and market demand, and is closely monitored throughout the holding period.

Cash Yield or Cash on Cash (COC)

Periodic income distributions as a percentage of invested capital. Also common in private credit, real assets, and infrastructure.

Real Estate: Strategies and Asset Types

Real Estate Strategies

Private RE strategies are typically categorized by their risk and return profile, from lowest to highest risk:

Core: stable, fully leased properties in prime locations, lowest return.

Core-Plus: mostly stable with minor improvements needed.

Value-Add: meaningful improvements needed to unlock income potential, often including tangible improvements or lease-up (filling vacant space to stabilize occupancy and income).

Opportunistic: ground-up development or major repositioning, highest risk and potential return.

Real Estate Asset Types

Real estate funds invest across a range of property types:

Multifamily: apartment buildings and residential rental properties, driven by housing demand and population growth. Typically one year lease terms.

Industrial: warehouses, distribution centers, and logistics facilities, benefiting from e-commerce and supply chain trends.Typically 5-20 year lease terms.

Office: commercial workspace, historically stable but facing headwinds from remote/hybrid work. Typically 5-15 year lease terms.

Retail: shopping centers, strip malls, and standalone stores, highly variable depending on tenant quality and location. Typically 5-10 year lease terms.

Self-Storage: individual storage units, known for low maintenance costs, recession resilience, and operational simplicity. Typically month-to-month lease terms.

Hospitality: hotels and short-term rentals, highly cyclical and sensitive to economic conditions.

Secondaries

See our Secondaries Investment Guide.

Secondary Investment

The purchase of an existing LP interest in a private fund, rather than investing in a newly formed fund. There are two types: LP-led (an existing investor sells their stake, often at a discount, to get liquidity before the fund's natural end) and GP-led (a GP moves assets into a new vehicle to extend ownership, typically at or near NAV with a smaller discount than LP-led).

LP-Led

A secondary transaction where an existing LP sells their interest in a fund to a new buyer before the fund's natural end date. LPs typically sell at a discount to NAV to attract buyers and achieve liquidity. Common motivations include portfolio rebalancing, liquidity needs, or exiting a manager relationship.

GP-Led / Continuation Vehicle

A secondary transaction initiated by the GP. The most common structure is a continuation vehicle, where the GP transfers assets from an older fund into a new vehicle, giving existing LPs the option to cash out or roll over ownership into the new vehicle. Ideally used to extend ownership of a fund's best-performing assets past its original term.

NAV Discount

Secondaries are often purchased at a discount to the fund's Net Asset Value (NAV), a key source of value in LP-led secondary investing. In practice, buyers may pay between 5-20% less than the stated value of what they’re buying.

The n-Curve

The counterpart to the J-Curve in secondary investing. Because secondary funds buy assets at a discount to NAV, early investors often see strongly positive early returns as the fund marks up to fair value (resembling a lowercase “n”), the inverse of the J-Curve's initial negative dip.

Where To Go From Here

Long Angle members can reach out to the Long Angle Investments team with any questions.

Non-members can learn more about Long Angle at longangle.com and apply for membership here.

See our Private Markets Glossary for a searchable list of private markets terms and definitions.

Ready to connect with like-minded peers navigating similar wealth decisions?

Join Long Angle, a private community where successful entrepreneurs, executives, and professionals collaborate on wealth strategies, investment opportunities, and life's next chapter.