The Boglehead 3 Fund Portfolio: Does the Strategy Change When the Numbers Get Bigger?

Written By: Scott Nixon

Updated June 2026

2025 High-Net-Worth Asset Allocation Study

See how high-net-worth investors are allocating across public equities, private companies, real estate, bonds, and alternatives. Based on benchmark data from investors where public equities average 47% of the portfolio.

The Boglehead 3 fund portfolio (U.S. total market, international total market, total bond market) is one of the most widely followed frameworks in personal finance. The question that surfaces repeatedly among Long Angle members who have reached significant wealth is not whether the strategy works. It is whether someone at that level is supposed to be doing something more. The answer, in most cases, is no. But the reasoning matters more than the conclusion.

The Boglehead 3 fund portfolio combines a U.S. total stock market fund, an international stock market fund, and a total bond market fund. For investors at any wealth level, the framework holds: low costs, broad diversification, and a structure that requires minimal ongoing decisions. A subset of Long Angle members at the $5M to $50M level run a Boglehead core alongside selective private market allocations rather than replacing one with the other.

Key Takeaways

The 3-fund portfolio scales with net worth. The philosophy does not require modification just because the dollar amounts grow.

Most Long Angle members who use a Boglehead core do so alongside private markets, real estate, or direct indexing. Not instead of them.

The bonds question is context-dependent. Bonds behaved unusually in the 2020-2022 rate environment; in a normal rate environment the diversification logic holds.

Dividend ETFs like SCHD are not a bond replacement. Correlation data shows SCHD tracks equities closely, not fixed income.

Every alternative investment adds decision overhead, tracking, and tax complexity without a guaranteed return premium.

Defining "enough" before building portfolio complexity is the decision that members at the post-exit stage most consistently say they wish they had made earlier.

What the Boglehead 3 Fund Portfolio Is

The Boglehead 3 fund portfolio holds three broadly diversified, low-cost index funds: a U.S. total stock market fund, an international total stock market fund, and a total bond market fund. Together, they provide exposure to thousands of securities across global markets with minimal fees and no need to select individual securities.

Inspired by Vanguard founder John C. Bogle, the philosophy rests on a few durable principles: minimize costs, diversify broadly, maintain a long-term perspective, and resist the urge to overcomplicate. Bogle's core argument was that the market is extremely difficult to beat consistently, so the rational move is to own it at the lowest possible cost.

The most commonly cited implementation uses Vanguard funds:

U.S. Total Stock Market Index Fund Admiral Shares (VTSAX) for U.S. equity exposure

Total International Stock Index Fund Admiral Shares (VTIAX) for international equity exposure

Total Bond Market Index Fund Admiral Shares (VBTLX) for fixed income

Equivalent ETFs (VTI, VXUS, BND) work identically for taxable accounts.

The ratio across the three funds is a personal decision. A younger investor might hold 80% in equities split between domestic and international and 20% in bonds. Someone approaching or in retirement might shift toward a more conservative allocation like 60/40. The exact split matters less than the discipline of maintaining it.

The Efficient Market Hypothesis, which underpins much of Boglehead thinking, holds that publicly available information is already reflected in prices, making consistent outperformance through security selection or market timing extremely unlikely over long periods. The 3-fund portfolio operationalizes this view without requiring an investor to forecast anything.

Beyond Wealth Newsletter

Weekly perspectives on wealth, investing, and the decisions that come after the financial ones get easier. Read by founders, executives, and investors navigating the same questions covered in this post.

The Core Question as the Portfolio Grows: Should You Be Doing More?

The Boglehead philosophy does not change because the dollar amounts change. This is the most consistently repeated insight across Long Angle discussions on the topic.

The question itself is understandable. Someone who has worked for two decades building a business, reached a high 8-figure net worth, and now holds tens of millions in managed brokerage accounts starts to wonder whether the simplest approach is really appropriate for their situation. As one Long Angle member put it after a significant exit: "The Boglehead approach seems to offer the least mental bandwidth and predictable outcomes, yet I somehow think, possibly wrongly, at our net worth we are way beyond that and should be doing 'more.' Is this 'more' just the greed and ego whispering?"

The responses were nearly unanimous, and they came from people at the same wealth stage.

One member who had gone through a similar experience described unwinding his private investments over several years: "I was adding complexity when I thought I was missing out on something. Maybe was missing on some returns, although not as obvious as you would think, and definitely was adding complexity." He now uses a spreadsheet to rebalance and does not think about it otherwise.

Another member framed it as a structural observation: at every stage of net worth, from $1M to $100M, there is a persistent sense that you should be doing something different. There are also service providers at every stage ready to agree with you and sell you something.

The counter-argument deserves honest treatment. One member pushed back: "Within any realm of plausible net worths, there is stuff I'd enjoy about having 3X as much, if I'm being totally honest." That is a reasonable position. The Boglehead philosophy is not an argument against having more. It is an argument about whether the added complexity reliably produces more, and whether the cost in time, stress, and overhead is worth whatever premium is generated.

A useful way to think about it: imagine two scenarios over ten years. In one, you hold a Boglehead portfolio, sleep well, and spend a few hours a year on investment decisions. The portfolio gains $10M. In the other, you pursue a more complex strategy: all the deals, alternatives, private credit, additional real estate. It takes more time. There is more anxiety. But it works and the portfolio gains $20M. The question is what that extra $10M changes about your life, and whether the gain is guaranteed or merely possible.

A Long Angle member cited the 2016 Wall Street Journal profile of Nevada’s pension manager and summarized the scaling argument this way: "Even at 9 figures, I don't think anyone needs to do more with their portfolio. Save the 'complexity budget' for estate planning, wealth transfer, and tax mitigation strategies."

The decision about whether to add complexity should start with a definition of what that complexity is supposed to accomplish. If the goal is already achievable with a simple portfolio, the case for adding complexity is harder to make.

How Long Angle Members Run It

The members who describe themselves as Boglehead investors rarely run a pure 3-fund portfolio without any adaptation. The more common pattern is a Boglehead core with pragmatic additions based on individual circumstances.

Across Long Angle discussions, a few allocation patterns appear repeatedly:

Some members hold nearly all liquid assets in two or three index funds. One member with a significant exit described holding 95% in VTI and VXUS with 5% in cash. No bonds. No private markets. The reasoning: the portfolio already exceeded what was needed for any plausible spending scenario, and simplicity was worth more than optimizing for additional return.

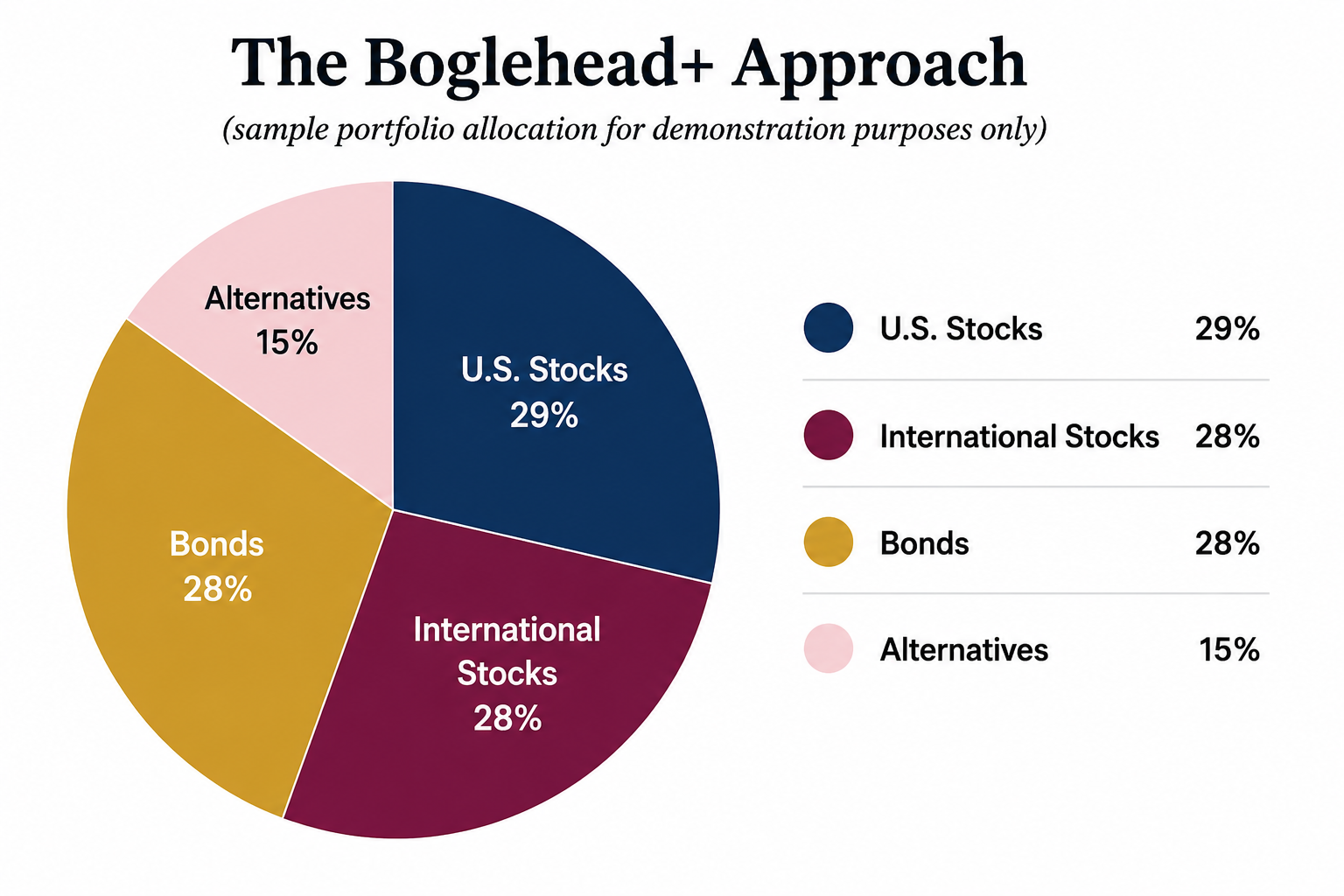

Others run what members have called a "Boglehead+" approach: an index fund core representing 80% to 90% of the liquid portfolio, with 10% to 15% in alternatives ranging from gold funds to private investments. The additions are intentional and bounded, not a drift into complexity. The index core is the foundation; the alternatives are an overlay.

A common real-world variation replaces bond exposure with real estate. Members who own investment property tend to treat the cash flow from those holdings as performing the same portfolio ballast function that bonds are supposed to provide. Whether that substitution holds under stress is a legitimate question the bonds section addresses.

Others, particularly those in or near retirement, hold genuine three-fund allocations with meaningful bond exposure. A 70/30 equity-to-bond split at $10M or $20M is not a conservative concession. For someone spending $300K a year with houses paid off, it may be the most rational structure available.

The allocation question every member in these discussions eventually asks is the same: what is the goal? If the portfolio needs to support a specific spending level and protect against a sequence of bad early returns, that is a different optimization than if the portfolio is a multigenerational asset where short-term volatility is irrelevant. Most of the variation in how members run the framework traces back to different answers to that question.

The Bonds Question

The most contested element of the 3-fund portfolio, at least among Long Angle members, is the bond allocation. The 2020-2022 period made this debate more acute.

BND, Vanguard's total bond market ETF, lost approximately 12.5% in 2022 as the Federal Reserve raised interest rates at the fastest pace in decades. For investors who had held bonds as a portfolio stabilizer, watching them decline alongside equities was disorienting. Some members sold their bond positions and moved to T-bills, unable to see a near-term reason to go back.

This reaction is understandable, but the conclusion it leads to deserves scrutiny. 2022 was historically anomalous. Bonds and equities have rarely declined together in the same year to that degree, precisely because bonds typically perform well in recessionary environments when the Fed is cutting rates rather than raising them. In a normal rate environment, the negative correlation between bonds and equities (the reason bonds belong in the portfolio) tends to reassert itself.

The implication for 3-fund investors is not that bonds were a mistake. It is that bonds in a zero-interest-rate environment were priced to deliver very little upside with meaningful downside if rates rose. In a more normal rate environment, the ballast function of bonds returns. Members who understand this distinction are better positioned to hold their bond allocation through a stress event rather than abandoning it at the worst time.

A separate question is whether dividend ETFs like SCHD can substitute for bonds. The answer from community discussions is consistent: no. The correlation between SCHD and VOO is approximately 0.91 in recent data shared in Long Angle discussions. The correlation between BND and VOO over the same period is approximately 0.36. Dividend-paying companies are still equities. They tend to fall with the broader market during risk-off periods, which is exactly when portfolio ballast matters most.

One Long Angle member with experience writing about portfolio construction identified the key risk for anyone holding a high-equity retirement portfolio without bonds: sequence of returns risk. A significant drawdown early in the drawdown phase, when withdrawals are large relative to the portfolio, causes permanent damage that a subsequent recovery cannot fully repair. Bonds, or another genuinely uncorrelated asset, reduce that risk in a way that dividend ETFs do not.

The takeaway from these discussions: if you are still accumulating and have a long time horizon, bond exposure is optional and the tradeoff is real (lower expected returns for lower volatility). If you are in or approaching the drawdown phase, genuine fixed income diversification is not optional. The goal is not to maximize the return line; it is to ensure the portfolio survives a bad sequence at the worst possible time.

Where do investors at the $5M to $50M level compare notes on how much to keep in a Boglehead-style core versus private credit, real estate, or equity?

Long Angle is a vetted community where members with no commission motive discuss portfolio construction, asset allocation, and what peers at the same wealth stage are doing. The environment is solicitation-free. Recommendations come from firsthand experience, not product relationships.

When Investors Adapt the Framework

The 3-fund portfolio was designed for public markets: liquid, broadly diversified, low-cost asset classes where the Efficient Market Hypothesis applies most reliably. At higher wealth levels, several adaptations are worth considering. None of them abandon the Boglehead core; they extend it.

Direct indexing is the most significant evolution for taxable accounts. Rather than holding a total market fund, direct indexing involves owning the underlying securities individually, which allows for tax-loss harvesting at the position level. An investor holding VTSAX cannot harvest losses within the fund without selling the fund. An investor holding the underlying stocks can harvest losses on individual positions that decline while the overall index rises, generating tax alpha without altering the portfolio's market exposure. Platforms have driven these costs down substantially, making direct indexing increasingly accessible below the $10M threshold where it was previously practical.

As one Long Angle member described it, the alternative for those who cannot or choose not to use direct indexing is: buying the largest-weight names in the S&P 500 alongside sector ETFs to approximate the index return while maintaining harvesting flexibility. It is more complexity than a pure index fund, but it produces most of the tax benefit with a fraction of the infrastructure.

Private markets are the other common addition. Members in these discussions largely agree that private equity, private credit, and real estate can complement the Boglehead core rather than replace it. The argument for including them is that private markets operate under different dynamics than public markets: less pricing transparency, less liquidity, and access barriers that create return opportunities not available to any buyer. A fund that underwrites at a 25% IRR is not going to be instantly arbitraged to zero the way a mispriced public security would be.

The argument against over-allocating to private markets is equally important. Illiquidity is a real cost. Capital call timing can create cash management complexity. Vintage risk means that a heavily committed private portfolio during a bad vintage may underperform a simple index fund for a decade. Long Angle members who describe themselves as primarily Boglehead investors and have experimented with private markets often conclude that private allocations of 10% to 20% of the portfolio are worthwhile, while allocations larger than that introduce more complexity and illiquidity than the expected return premium justifies.

For investors with significant concentrated stock positions, donor-advised funds provide a clean way to integrate charitable intent with the Boglehead framework. Contributing appreciated securities to a donor-advised fund allows the donor to avoid realizing the embedded capital gain while still supporting charitable goals. For investors already inclined to give, this is often the most tax-efficient move available, and it fits naturally within a simplified, low-turnover portfolio approach.

Across all these adaptations, the Boglehead core remains the foundation. The index holdings provide the liquidity, the diversification, and the simplicity that allow the non-core positions to be managed with appropriate time and attention.

Finding Enough

The question underneath most Boglehead discussions among high-net-worth investors is not really about portfolio construction. It is about what the portfolio is supposed to do.

John C. Bogle wrote a book called Enough. In it, he recalled a story about Kurt Vonnegut and Joseph Heller at a party hosted by a billionaire. Vonnegut mentioned that their host had made more money in a single day than Heller had earned from Catch-22 over its entire history. Heller responded: "Yes, but I have something he will never have. Enough.”

For a Long Angle member who has already had a significant exit, the question becomes: what does additional return change? One member laid it out plainly, comparing the Boglehead scenario with the more complex one over ten years. The $10M difference in the complex scenario buys another family foundation, another vacation home, possibly private aviation. The question is whether that incremental wealth changes life satisfaction in proportion to the time, stress, and complexity required to pursue it.

Most members who had gone through this calculation and landed on simplicity described a version of the same thing. There is a persistent anxiety that comes with more complex investing. There is also a point at which monitoring positions, fielding capital calls, reviewing quarterly reports, and managing tax complexity takes up the mental space that used to be occupied by other things.

One discussion participant put the investment case for simplicity: "Every investment is also a new drain on your mental energy in terms of deciding, tracking, and reporting. It's not clear to me that I could outperform index funds even if I tried, but I will consider the missed alpha an investment in myself, giving me more time to work on something meaningful where I do believe I have an edge."

The SWAN principle, which stands for sleep well at night, captures something real. A portfolio you do not have to worry about has a value that does not appear in any spreadsheet. For investors who have already reached financial independence, the relevant question may not be how to maximize the return. It may be how to build a portfolio that supports the life they want without requiring ongoing attention.

One member summarized the framework his investment policy statement uses: LADS. Low cost, automatic, diversified, straightforward.

Questions to Ask Before Adding Complexity

Before deviating from a Boglehead core, a set of honest questions can help clarify whether the deviation is a genuine improvement or a response to the same pressure that exists at every wealth level.

Does my annual spending require returns above what a diversified index portfolio can produce? If a 6% to 7% annualized real return covers spending with significant cushion, then strategies targeting 10% to 15% are solving a problem that does not exist.

Do I want to hold assets outside the two main public market asset classes (equities and bonds)? Real estate, private equity, and private credit can provide genuine diversification if approached thoughtfully. The question is whether the exposure is intentional or driven by FOMO.

Is the Boglehead approach tax-efficient given my specific situation? For investors with large concentrated positions, significant unrealized gains in existing funds, or complex income situations, direct indexing or other tools may provide meaningful tax improvement over a standard 3-fund approach.

Would a non-Boglehead approach be more complicated, and is that complication worth the potentially higher return? Complexity is not free. Every alternative investment is a decision, a tracking obligation, a tax reporting event.

What is the cost of starting with a Boglehead approach and pivoting later? Transitioning out of a Boglehead portfolio that has appreciated significantly may require realizing substantial gains. Understanding the exit cost before building a position matters.

These questions do not produce a universal answer. They produce an honest one.

Frequently Asked Questions

What are the three funds in the Boglehead 3 fund portfolio?

The three funds are a U.S. total stock market fund, an international total stock market fund, and a total bond market fund. The most widely used Vanguard implementations are VTSAX, VTIAX, and VBTLX. Equivalent ETFs (VTI, VXUS, BND) perform identically in taxable accounts and offer slightly lower expense ratios.

Does the Boglehead strategy work at higher net worth?

Yes. The framework scales because its advantages (low costs, broad diversification, minimal decision overhead) do not diminish as the portfolio grows. The Nevada State Investment Council, profiled in the Wall Street Journal, ran over $50 billion using index-based strategies with a similar philosophy. Long Angle members with high 8-figure portfolios run the same core.

Can I replace bonds with dividend ETFs like SCHD?

No, not as a direct substitute. Dividend ETFs are equity instruments. SCHD's correlation to VOO is approximately 0.91 based on recent data. BND's correlation to VOO over the same period is approximately 0.36. The function bonds serve, providing ballast when equities fall, requires an asset that moves independently of equities. Dividend-paying companies do not reliably do that.

What is the difference between VOO and VTI?

VOO tracks the S&P 500, covering the 500 largest U.S. companies. VTI tracks the entire U.S. market including mid-cap and small-cap companies. Both work in a Boglehead framework. VTI provides slightly broader diversification. The performance difference over long horizons has been small, though some members who follow research on small-cap value tilts prefer VTI's broader coverage as a starting point for more deliberate factor exposure.

Do Boglehead investors use private markets?

Many do, as a complement to the index core rather than a replacement. The typical pattern among Long Angle members is a Boglehead foundation in public markets with 10% to 20% in private equity, private credit, or real estate for additional diversification. The Boglehead core provides the liquidity and stability that allow less liquid private allocations to be held without stress.

What is direct indexing and how does it relate to the Boglehead approach?

Direct indexing replicates an index by holding the underlying stocks individually rather than through a fund. This allows tax-loss harvesting at the individual position level, which a fund investor cannot do. For high-net-worth investors, direct indexing is a tax-efficient evolution of the Boglehead approach rather than a departure from it. The goal and the exposure are the same; the structure provides more tax flexibility.

When do bonds make sense in a Boglehead portfolio?

Bonds provide ballast: they tend to hold value or appreciate when equities fall in a recessionary environment. The case for bonds is strongest for investors in or approaching the drawdown phase, where sequence of returns risk is a real concern. For long-horizon accumulators who can tolerate short-term volatility, bonds are optional. The 2022 rate cycle was unusual; in a more normal interest rate environment, the negative correlation between bonds and equities that motivates including them tends to hold.

Final Thoughts

The Boglehead 3 fund portfolio is not a beginner's strategy that investors graduate out of as their wealth grows. It is a framework built on principles that hold across wealth levels: own the market, minimize costs, stay the course, and avoid the temptation to overcomplicate.

For most Long Angle members who have reached significant wealth through a business exit or professional success, the real question is not whether the portfolio is sophisticated enough. It is whether complexity that gets added will improve outcomes or will mainly serve as a response to the persistent feeling that someone at their level should be doing more. The answer, in most cases, is that the feeling is not a reliable guide.

A Boglehead core alongside thoughtful allocations to private markets, direct indexing for tax efficiency, or real estate for cash flow diversity is a reasonable architecture for many investors in this wealth range. What rarely makes sense is adding complexity for its own sake, or because the complexity sounds more appropriate to the dollar amounts involved.

Simplicity is not a compromise. It is a structural choice with real advantages that compound over time.

Most advisors benefit when you add complexity.

Long Angle is a vetted community where members with no commission motive discuss whether simplicity still makes sense as the portfolio grows, and what peers with significant exits have done with theirs. The community spans 8,000+ vetted members, covers financial and lifestyle decisions in the same place, and operates without advisors or salespeople in the room.

If you are building wealth at the $2.2M+ level and want access to candid peer discussions on portfolio construction, asset allocation, and what the path from here looks like, apply today.

More From Long Angle

Beyond Wealth Newsletter

Long Angle's free weekly newsletter covering wealth management, investing, and life at the intersection of money and ambition. Subscribe »

Navigating Wealth Podcast

The Long Angle podcast. Founders and executives on the financial and personal decisions that matter most. Listen »