Hedge Fund Minimum Investment: What It Takes to Get In

Written By: Ryan Morrison.

Based on a Navigating Wealth conversation with Megan Nicholson.

2026 High-Net-Worth Asset Allocation Report

See how high-net-worth investors with an average net worth of $17M are allocating across public equities, private markets, real estate, bonds and cash. Based on benchmark data from 230+ respondents.

Hedge funds were supposed to be fading. Megan Nicholson has spent two decades on the other side of that assumption, first raising institutional capital for hedge fund clients at Lehman Brothers, Barclays, and Jefferies, then helping emerging managers position themselves to allocators at her firm, ImgArb. The data she sees daily tells a different story than the popular narrative: 2025 brought the largest hedge fund inflows in a decade. The harder question for an individual investor is not whether hedge funds are relevant. It is what it takes to get access to a good one.

Hedge fund minimums vary widely by strategy and manager stage. Friends-and-family rounds for new managers can start as low as $1 to $2 million in aggregate, while institutional-grade funds often require $5 million or more per investor. Larger, established multi-strategy platforms typically set minimums well above $1 million and may be effectively closed to individual investors outside family offices and institutions.

Key Takeaways

Hedge funds saw $116 billion in inflows in 2025, the largest in a decade, driven mainly by niche, sector-specific strategies rather than generalist long-short equity

Fees are broadly compressing: the 2025 average ran roughly 2% management and 18.5% performance fee, down from the traditional 2-and-20, though premium multi-strategy platforms still command higher, less negotiable terms

New hedge fund managers raise capital through a defined progression: friends and family, former colleagues and high-net-worth individuals, family offices, then institutional allocators

The strongest diligence signal is repeatability over three or more years, not short-term outperformance

Red flags include an inability to articulate differentiation quickly and pitch decks that emphasize marketing over substance

Table of Contents

Hedge Funds Are Not Fading, They Are Specializing

The popular narrative is that hedge funds peaked years ago, that the easy money left when equity markets started their long climb and never looked back. The numbers say otherwise. Hedge fund assets under management exceeded $5 trillion in 2025, and the industry recorded $116 billion in net inflows that year, the largest annual inflow in a decade.

The growth is not evenly distributed. The renewed interest is concentrated in niche, sector-specific strategies rather than generalist long-short equity funds tracking the broad market. Allocators are increasingly drawn to healthcare-focused funds, metals and mining specialists, and managers with deep expertise in a narrow vertical, somewhat less so in energy and broad technology, media, and telecom strategies that dominated prior cycles.

The thesis behind this shift is straightforward. Institutional investors want exposure to specific sectors and geographies with some measure of downside protection, rather than a generalist manager attempting to do everything reasonably well. A manager who has spent a decade studying a single niche, one nobody on Wall Street is covering closely, offers something a broad-market long-short fund cannot: genuine information advantage in a narrow space.

Watch the Full Conversation

This article draws on a Navigating Wealth conversation with Megan Nicholson, where we discuss what is really happening in hedge fund allocation trends, how fee structures are shifting, and what it takes for an individual investor to access and evaluate a credible manager. Watch the full episode for the broader discussion.

Subscribe on YouTube · Get weekly episode updates

Megan Nicholson is a partner at ImgArb, a boutique firm that helps investment managers across hedge funds, private equity, real estate, and venture capital raise institutional capital through positioning, branding, and pitch materials. She began her career on the capital introductions desk at Lehman Brothers in 2005, later working at Barclays and Jefferies before co-founding ImgArb, giving her two decades of direct visibility into how allocators evaluate managers.

What Hedge Fund Minimums Look Like

Hedge fund minimums depend heavily on where a manager sits in their fundraising lifecycle, which makes a single universal number misleading.

New managers frequently launch with $1 million to $2 million of their own capital plus contributions from friends and family, then work to raise additional commitments from there. What counts as a meaningful launch has shifted upward in recent years. A "larger launch" in the current market typically starts around $100 million, and a small number of well-connected managers can launch with $1 billion or more from day one. Most new entrants fall well short of that.

Minimums for individual investors scale accordingly. An emerging manager building a track record may accept smaller checks, sometimes in the low six figures, specifically because they need committed capital to demonstrate viability. An established multi-strategy platform with a multi-decade track record will set minimums well above $1 million, often with limited capacity even for investors who meet that threshold, since these platforms are frequently oversubscribed.

The realistic path for an individual investor depends on identifying where a manager sits on this spectrum and matching expectations accordingly. A $5 million investor pursuing access to a large, established multi-strat platform is fighting a different battle than the same investor evaluating a credible emerging manager three years into their track record.

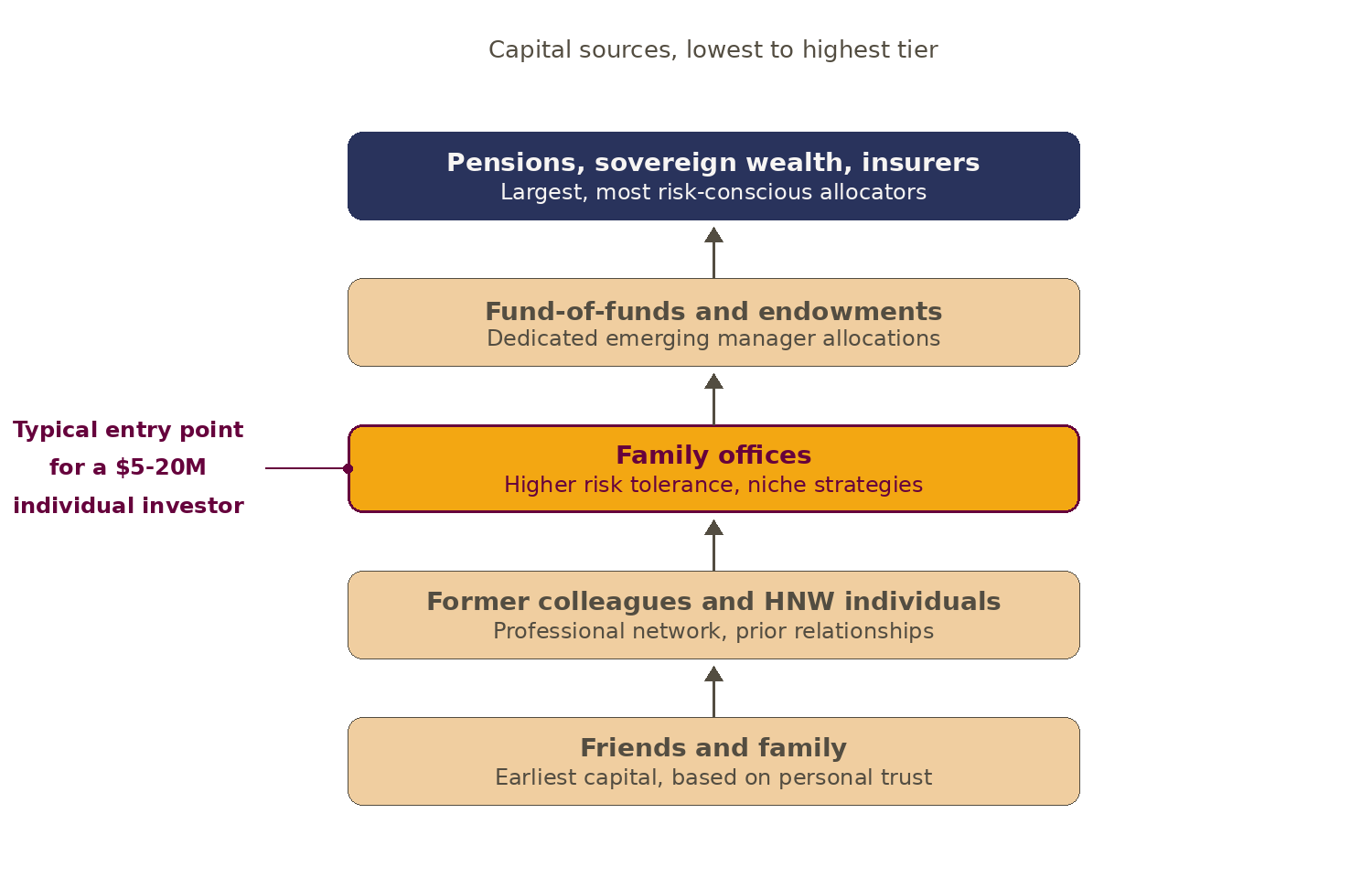

The Capital-Raising Food Chain

Hedge fund managers raise capital through a fairly consistent progression, and understanding it clarifies where individual investors realistically fit.

The earliest capital comes from friends and family, people willing to back a manager based on personal relationship and conviction rather than an established record. From there, managers typically move to former colleagues and high-net-worth individuals within their professional network, often people who worked alongside them at a prior fund or firm.

Family offices and multi-family offices represent the next tier. Because of how that wealth was typically created, family offices tend to carry a higher risk tolerance than institutional allocators and show more willingness to back niche, specialized strategies that a generalist endowment might pass on.

Beyond family offices sit fund-of-funds and endowments with dedicated allocations for emerging managers, some of which will commit capital to funds as small as $5 million in assets. From there, the ladder continues upward to pensions, sovereign wealth funds, and insurance companies, the largest and most risk-conscious allocators in the market.

For an individual investor with $5 million to $20 million in investable assets, the realistic point of entry sits closer to the high-net-worth and family office tiers than the institutional tier. That positioning matters because it shapes which managers are accessible and which require a credibility threshold most individual investors have not yet cleared.

Beyond Wealth Newsletter

Weekly perspectives on money, meaning, and the decisions that come after the financial ones get easier. Read by founders, executives, and investors navigating the same questions covered in this post.

Hedge Fund Fee Structure: What 2 and 20 Costs in 2025

The traditional hedge fund fee structure of 2 and 20 means a 2% annual management fee on assets plus a 20% performance fee on profits. That standard has been eroding for years, and 2025 data shows just how far.

The 2025 average landed at roughly 2% management and approximately 18.5% performance fee, a meaningful step down from the traditional structure. Pass-through fees to investors have declined broadly, and the trend favors more investor-friendly terms across the standard hedge fund universe.

| Fee Tier | Management Fee | Performance Fee | Notes |

|---|---|---|---|

| Traditional 2 and 20 | 2% | 20% | The historical industry standard |

| 2025 Industry Average | ~2% | ~18.5% | Broad fee compression across standard funds |

| Multi-Strategy Platforms | 2%+ (often pass-through) | 20%+ | Premium terms largely unchanged; investors accept higher costs for consistent net returns |

That compression is not universal. Multi-strategy platforms, the large, professionally managed pod-shop style funds that allocate capital across many internal teams, have largely held their ground on fees, in some cases charging more than 2 and 20 through pass-through cost structures that bill investors for the platform's full operating expenses. Investors continue to pay these premium terms because the net returns, often in the 13% range after fees, have proven durable across market cycles. A manager generating 25% to 30% gross returns consistently can absorb a heavier fee load and still deliver an attractive net result.

A related shift is reshaping how larger allocators negotiate terms entirely. Institutions willing to commit significant capital, often $100 million or more, increasingly request separately managed accounts (SMAs) rather than standard fund commitments, sometimes paired with a GP stake in the management company itself. For an emerging manager, this creates a genuine trade-off: accepting an SMA or GP-stake arrangement brings committed capital and often valuable operational and marketing support, but it also means giving up a piece of long-term ownership in the business being built.

Types of Hedge Fund Strategies Worth Knowing

The hedge fund category covers a wide range of approaches, and the strategy matters more than the "hedge fund" label itself.

Equity market neutral strategies aim for close to zero net exposure, holding long and short positions in roughly equal measure to isolate stock-specific returns from broad market movement. Long-short equity strategies with a specific sector focus take a directional view while using shorts to manage risk, rather than attempting true market neutrality. Event-driven and quantitative long-short approaches each apply a more systematic process to identifying opportunities, whether around corporate events or model-driven signals.

Multi-strategy platforms diversify across many of these approaches simultaneously under one institutional umbrella, professionally managed with deep operational infrastructure, but as covered above, they typically carry the highest and least negotiable fee structures in the category.

Global macro funds and niche sector specialists, particularly in healthcare and metals and mining, represent where much of the renewed 2025 interest has concentrated. The common thread across the strategies gaining the most allocator attention right now is specificity: a clearly defined edge in a narrow space, rather than a generalist approach to broad market exposure.

How to Evaluate a Hedge Fund Manager

The single most important signal in evaluating any hedge fund manager is repeatability, not short-term performance. A manager who can show consistent results across three or more years, including the periods when the strategy struggled, has demonstrated something a single strong year cannot: that the process holds up when conditions are unfavorable, not only when they are favorable.

Consistency through both gains and losses is the underlying test. A manager who quietly diverges from their stated process the moment markets get volatile is signaling something important about how they will behave with real capital at stake. The strongest managers maintain discipline in both directions.

Quantitative diligence (return streams, drawdown analysis, exposure data) only tells part of the story. The qualitative layer matters just as much: getting to know the person managing the capital, understanding how they think under pressure, and building enough of a relationship to ask direct questions and trust the answers. Reputation among other investors who have worked with the manager carries real weight here, often more than anything in a pitch deck.

A practical test that separates strong managers from weak ones: can they explain what makes them different in twenty seconds or less? Managers who cannot articulate their edge quickly and clearly often have not fully clarified it for themselves. Red flags include pitch materials that lean heavily on marketing language without substantive detail on the actual investment process, and any framing that resembles retail-style promises rather than the measured, specific language institutional allocators expect.

Where do members compare notes on which hedge fund managers are worth a serious look?

Long Angle is a vetted community where members discuss alternative investment opportunities, including the niche, specialist managers that rarely show up in mainstream financial advice. The environment is solicitation-free, with peer experience driving every recommendation rather than a commission.

Why Individual Investors Struggle to Access This Market

The biggest obstacle for an individual investor in this space is not capital. It is information.

Reliable, current intelligence on niche hedge fund strategies is genuinely hard to find. Public sources tend toward generic explanations of what a hedge fund is, not which managers in a specific sector have a credible, repeatable edge right now. Traditional wealth advisors are frequently under-equipped to diligence specialist strategies outside their usual scope, particularly in narrower verticals like sector-specific long-short or niche event-driven approaches.

Before structured peer networks existed in this space, individual investors largely relied on informal channels: their own professional network, secondhand accounts from people they trusted, and inconsistent signals about which managers were worth a serious look. That approach worked for some, but it left most investors without a reliable way to access or evaluate managers operating in genuinely specialized strategies.

Pooled access combined with peer-vetted intelligence solves a real structural gap. When a group of high-net-worth investors can collectively evaluate a manager, share diligence findings, and pool commitments to meet institutional minimums, the access problem and the information problem are addressed at the same time. For founders and investors exploring other paths to alternative investment exposure beyond traditional fund structures, the same principle applies: specialized opportunities require specialized, trustworthy sources of information to evaluate properly.

Frequently Asked Questions

What is the minimum investment for a hedge fund?

Minimums vary widely. New managers may accept commitments in the low six figures while building a track record, while established multi-strategy platforms often require $1 million or more, frequently with limited capacity even for qualifying investors. The realistic minimum for a given investor depends heavily on which stage of fundraising a manager is in.

What is the standard hedge fund fee structure?

The traditional structure is 2 and 20: a 2% annual management fee plus a 20% performance fee on profits. As of 2025, the broader industry average has compressed to roughly 2% management and 18.5% performance fee, though large multi-strategy platforms have generally held firm on higher, less negotiable fee terms.

Is 2 and 20 still the norm for hedge funds?

It remains the reference point, but actual fees have compressed below it across most of the industry. Multi-strategy platforms are the notable exception, in some cases charging at or above the traditional 2 and 20 level through pass-through cost structures, and investors continue to pay those fees because of consistent net returns.

What is a multi-strategy hedge fund?

A multi-strategy hedge fund allocates capital across multiple internal teams running different strategies simultaneously, all under one institutional platform. These funds tend to be among the largest and most established in the industry, with correspondingly higher and less negotiable fee structures compared to single-strategy managers.

How do you evaluate a hedge fund manager before investing?

The strongest signal is a repeatable process demonstrated over three or more years, including periods of underperformance, not just strong recent results. Beyond the numbers, evaluating the manager as a person, their consistency under pressure, their reputation among other investors, and their ability to clearly articulate what makes their strategy different, matters as much as quantitative diligence.

Are hedge funds a good fit for a $5 to $10 million portfolio?

It depends on the specific strategy, the investor's risk tolerance, and access to credible managers. Hedge funds can offer genuine diversification benefits and exposure to niche strategies unavailable through public markets, but minimums and access constraints mean an investor at this level typically has a narrower set of realistic options than a family office or institutional allocator.

Final Thoughts

The hedge fund industry is not shrinking. It is becoming more specialized, with the strongest interest concentrated in niche strategies run by managers with genuine, narrow expertise. For an individual investor, the real obstacle has rarely been capital. It has been finding reliable information about which managers in a given niche deserve serious consideration.

That problem has a structural solution: pooled access and peer-vetted intelligence, evaluated by people who have no commission riding on the outcome.

Specialized strategies require specialized, trustworthy intelligence.

Long Angle is a vetted community where members compare notes on hedge fund managers, private equity opportunities, and other alternative investments, with no one in the room trying to sell a specific deal. Members share what they are seeing, what diligence revealed, and what they decided.

Watch or Listen

Watch on YouTube · Listen on Spotify · Apple Podcasts · Amazon Music