Wealth Migration: How Taxes Affect Moving Decisions Among High Earners

Written By: Chris Bendtsen

Based on Long Angle Investments research and the Stanford GSB Search Fund Study.

2026 High-Net-Worth Asset Allocation Report

See how high-net-worth investors with $2M-$100M+ are allocating across public equities, private markets, real estate, bonds, and cash. Based on benchmark data from 230+ respondents.

Wealth migration refers to the movement of high-net-worth individuals across state or national borders, often driven by a combination of financial, tax, lifestyle, and family factors. Recent headlines say it's increasing, with more high earners leaving high-tax states and more U.S. citizens looking abroad.

A Long Angle community poll of 200+ members puts peer-level numbers on the trend. The community discussion that followed surfaced what's driving the decision at the household level and where taxes fit in.

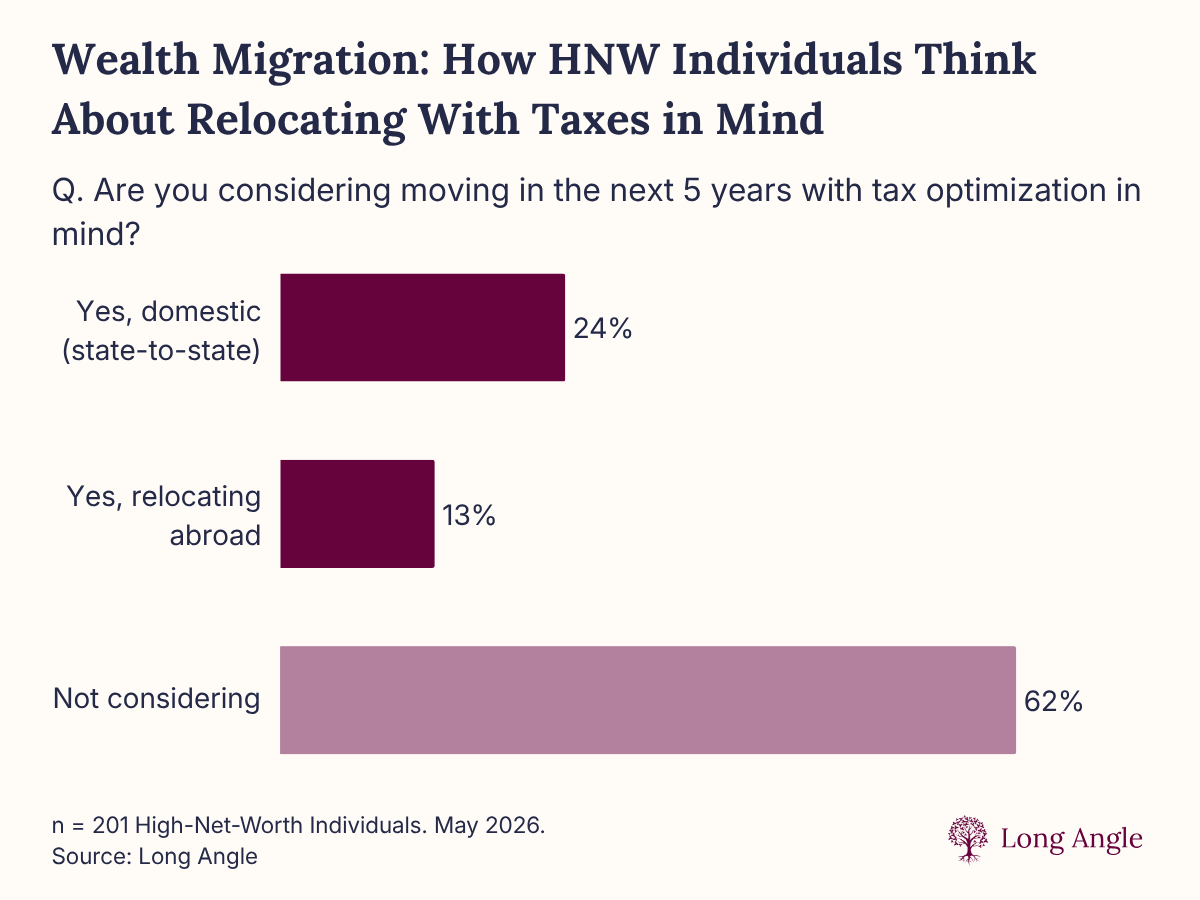

Wealth migration is an active planning question for high-net-worth individuals. In a recent Long Angle poll of 200+ members, 37% are considering a domestic or international move in the next five years with tax optimization in mind. While taxes rarely drive the relocation decision entirely, those who've made a move say the tax savings are hard to ignore.

Key Takeaways

24% of high-net-worth individuals surveyed are considering a domestic state-to-state move in the next five years with tax optimization in mind. 13% are considering relocating abroad.

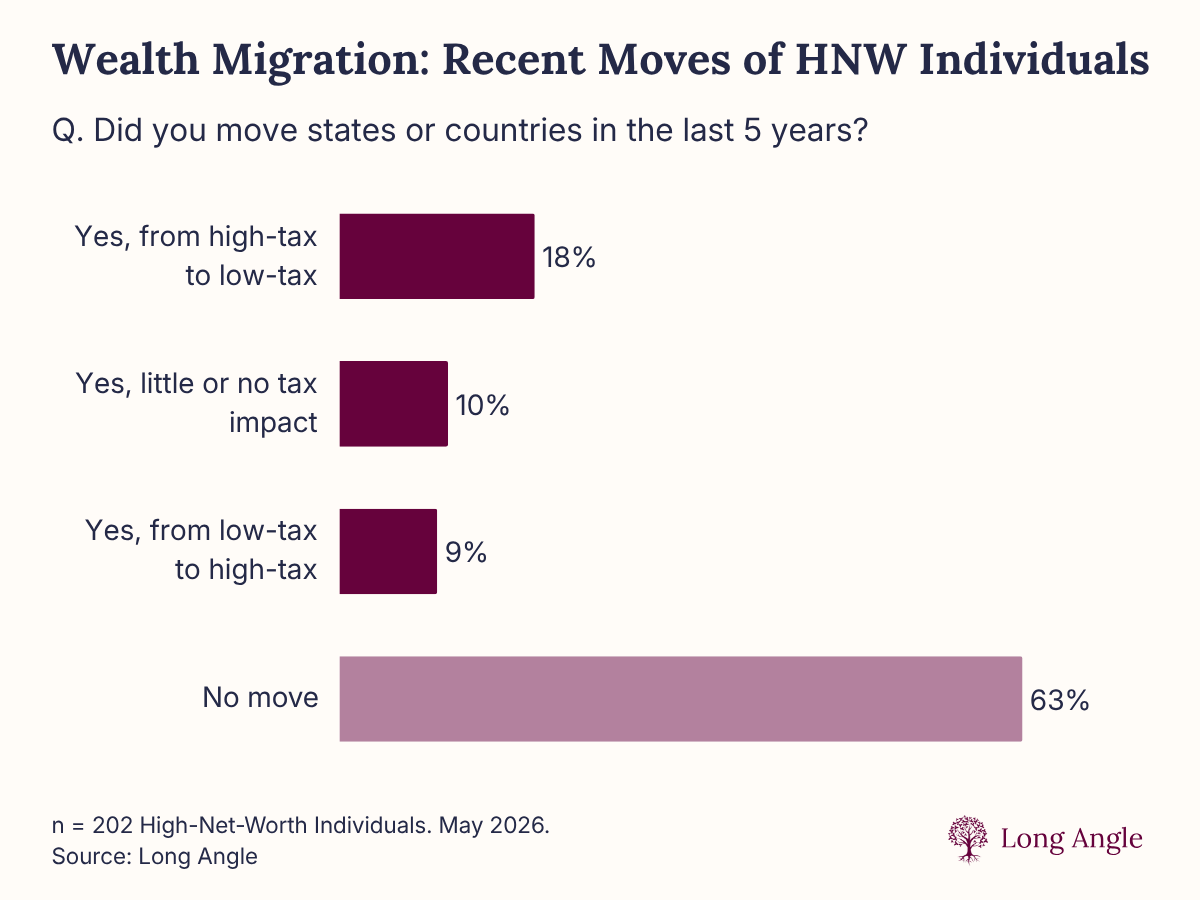

18% have moved in the last five years from a high-tax to a low-tax state.

Moving abroad for tax reasons carries a different and often more complex calculation than domestic relocation.

California has aggressive residency rules that can pursue former residents long after they leave. Timing a move relative to a liquidity event matters significantly.

How Taxes Influence Wealth Migration

Headlines increasingly point to tax policy as a driver of high earner relocation. Our Long Angle member poll asked two questions to understand how that's playing out in practice: whether members moved states or countries in the last five years, and whether they're considering a move in the next five years with tax optimization in mind.

On past moves, 18% relocated from a high-tax state (e.g., California, New York) or country to a lower-tax one (e.g., Texas, Florida) within the past five years. Note this question didn’t ask for a reason for the move.

On future plans, the picture shifts: 37% of 201 respondents are considering a move in the next five years with tax optimization in mind. That share breaks down to a quarter (24%) thinking about a domestic state-to-state move and 13% considering relocating abroad.

Most high-net-worth families aren't considering a move at all. And while the two poll questions aren't a perfect comparison (the first asked about moving, the second about considering with taxes in mind), the jump from 18% to 37% suggests a shift in mindset may be underway. For more high earners, tax implications are at the very least part of the home-base conversation.

The numbers establish that wealth migration is on the table for a sizable share of high earners. But they don't explain what tips the decision. That's where the discussion forum is more revealing.

Beyond Wealth Newsletter

Weekly perspectives on money, meaning, and the decisions that come after the financial ones get easier. Read by founders, executives, and investors navigating the same questions covered in this post.

What Drives Relocation Decisions

Member comments in the discussion thread show that the decision to move is almost never primarily about state taxes. Several members said any move would be driven by other motivations: work, lifestyle, and family.

Once a move is on the table, family considerations are weighed most heavily. Members discussed employment opportunities for a spouse or partner, proximity to family, and the cultural environment for family members before any tax calculation entered the conversation.

Still, others noted that once they moved, the calculus changes. One member who relocated from a high-tax state to a no-income-tax state more than a decade ago said taxes were not the reason for the move at the time, but the effects are real. If asked now to move back, they would have to think seriously about returning to a high marginal state income tax rate. Another member agreed strongly, saying, “I don’t think I’d ever move back because of cost of living and taxes.”

Where tax did enter the decision phase was in the choice of destination. One member shared that taxes were not the reason to leave, but were a definite factor in deciding where to end up. For others, tax considerations worked in the other direction, removing options rather than creating them. One member ruled out Canada and Italy entirely over their tax structures. In these scenarios, the decision to move came first, then taxes shaped which location made the most sense.

Interest in state-to-state mechanics is widespread in the community. When one member offered to share an analysis of which states to leave and which to move to for tax purposes, a long line of members asked for it.

States High Earners Are Leaving and Moving To

Among members who shared their moves, California, New York, and Connecticut were the most common departure states, and Texas, Florida, and Nevada were the most common destinations. Specific moves named in the thread included California to Texas, California to Hawaii then Florida, Connecticut to Nevada, and New York to Florida.

Common Departure and Destination States Among High Earners

| State | Relocation Pattern | Top Marginal Income Tax Rate |

|---|---|---|

| California | Departure | 13.3% |

| New York | Departure | 10.9% (plus NYC tax) |

| Connecticut | Departure | 6.99% |

| Texas | Destination | 0% |

| Florida | Destination | 0% |

| Nevada | Destination | 0% |

Sources: Long Angle member discussion. Tax rates per Tax Foundation, 2026.

These routes reflect the pattern in broader migration data. States with high marginal income tax rates, including California's top rate of 13.3% and New York City's combined state and city rates, have seen outflows of high-income households to states with no personal income tax, such as Florida, Texas, and Nevada. IRS migration data analyzed by the Tax Foundation shows high-tax states losing income-tax filers to no-income-tax states, with California and New York posting the largest net losses and Texas and Florida among the largest gains. For members comparing specific tax profiles across potential destinations, the Tax Foundation maintains current state income tax rate data.

Several members made the case that staying put is a perfectly reasonable financial decision, even when it isn't the optimal one. One member in Georgia pointed to the state's roughly 5% income tax rate and moderate property taxes, which place it in a middle range where the tax savings from a move would be marginal. Another said they would only relocate if a job made it necessary, with cost of living and tax profile as secondary considerations rather than the reason for the move. The discussion pointed to genuine community interest in detailed state-by-state comparison, but as a planning tool rather than a relocation trigger.

Moving Abroad Is a Different Calculation

For the 13% of high earners considering an international move with taxes in mind, the calculus is more complex than a domestic relocation. U.S. citizens are taxed on worldwide income regardless of where they live. So while state taxes are removed, moving abroad does not eliminate U.S. federal tax liability unless a person formally renounces citizenship. For most high earners considering a partial or full relocation abroad, the question is how to layer foreign tax obligations against U.S. ones, and whether the lifestyle benefit justifies the administrative complexity.

One member who had obtained EU citizenship was considering a part-time move there but noted they would not pursue a full relocation due to the tax environment. A different member noted that Portugal's rules on residency and capital gains can affect visitors who stay more than six months, even if they do not consider themselves tax residents. Another had applied for Canadian citizenship but noted Canada does not have a step-up in cost basis at death, a costly difference from U.S. law for households holding highly appreciated assets.

The IRS guidance on international tax obligations for U.S. citizens abroad covers a baseline framework, including the Foreign Tax Credit and foreign earned income exclusions available to those living outside the United States. Long Angle's partnerships include vetted advisors on international residency and citizenship options for members navigating this research. For anyone seriously evaluating an international move, a formal pre-departure tax review with both a U.S. tax attorney and a local advisor in the destination country is an appropriate starting point.

Where do peers who've already run the wealth migration math compare notes on what they found?

Long Angle is a vetted community where members pressure-test decisions like this one against people who have made the same call. The environment is solicitation-free: just firsthand experience from members with no incentive to sell you anything.

Tax Factors Worth Reviewing Before Planning a Move

Members weighing a move are thinking proactively about tax implications. Several noted they were tracking what a future year's income or a potential liquidity event might look like, and whether the timing of a move could change their tax exposure around it. For anyone evaluating a move, start here with your tax research:

State domicile and residency rules. Most states use a combination of where you maintain a permanent home, where you spend the majority of your time, and where your significant personal and business ties are concentrated to determine your tax domicile. Changing domicile typically requires more than a change of address: you generally need to vote, register vehicles, and update estate planning documents.

California's aggressive clawback rules. The California Franchise Tax Board applies residency rules that can follow former residents for longer than they expect. Per FTB Publication 1004 on equity-based compensation, stock options and RSUs granted while a person lived in California are sourced to California based on the ratio of California workdays during the vesting period, even if the options are exercised or shares vest after the move. Income from a California business and deferred compensation tied to California services can also remain subject to California tax after a move. Members with significant equity in California-based businesses or unvested California stock compensation should model the state-specific tax implications before and after a move, not just the income tax rate differential.

Timing around a liquidity event. One of the highest-leverage decisions a high earner can make around state taxes is timing a domicile change relative to a major liquidity event. Moving from a high-tax state before closing a business sale, exercising stock options, or receiving a large equity payout can produce significant savings. Moving after the event closes typically produces none. For members expecting a material liquidity event, this timing question belongs in the planning conversation well before the transaction.

Part-year residency mechanics. In the year of a move, most states require you to file as a part-year resident and allocate income to each state based on the portion of the year you lived there. The rules for sourcing income to a specific state vary: wages are generally sourced based on where you work, but investment income, capital gains, and equity compensation have their own sourcing rules that depend on the state. A high-net-worth accountant who has navigated multi-state residency situations is the right resource.

The broader tax picture. State income tax is just one variable. Estate and inheritance taxes, property taxes, and cost-of-living differences affect the full after-tax financial comparison. Understanding tax strategies relevant to your situation alongside a state relocation analysis gives a clearer picture of actual savings.

Read Long Angle’s New to Wealth Checklist to see the benefits of hiring a tax advisor who focuses on high-net-worth clients.

Frequently Asked Questions

What is wealth migration?

Wealth migration refers to the movement of high-net-worth individuals across state or national borders, often driven by a combination of tax, lifestyle, family, and economic factors. The term covers both domestic relocation (state-to-state moves within the U.S.) and international relocation.

Is it common for high-net-worth individuals to relocate for tax reasons?

Based on Long Angle member data, most do not. In a poll of 202 members, 63% had not moved in the last five years. Of those who had moved, lifestyle, family, employment, and personal considerations consistently ranked above taxes as the reason for moving. Tax influenced where members chose to land, not whether they moved in the first place.

Is it worth moving to a state with no income tax?

For most high earners, the answer depends on income level and type, the personal cost of moving, and whether the destination state is somewhere they want to live. Tax savings from moving from California to Texas, for example, are real. But whether savings justify the disruption depends on factors specific to the household.

What states do high earners tend to move to?

Texas, Florida, and Nevada are the most common destinations among Long Angle members who have moved from high-tax states. All three have no personal state income tax.

How does California handle residents who move to avoid state taxes?

California's Franchise Tax Board maintains residency rules that can apply to former residents for income earned while they still lived in California, including unvested equity and deferred compensation arrangements. Former residents with California-source income should not assume their California tax obligations end when they change their address. A qualified tax advisor with California nonresident experience should review the situation before and after any move.

When should I move relative to a major liquidity event to save on state taxes?

Generally, before the event closes and often well before. Changing your state tax domicile after a business sale, equity payout, or large capital gain event typically does not reduce tax on that event. The timing of a domicile change needs to happen before the income is recognized, requiring planning that begins months or years before the transaction.

What should high earners consider before moving abroad for tax reasons?

U.S. citizens owe U.S. federal tax on worldwide income regardless of where they live, so moving abroad does not eliminate federal tax liability. International relocation can layer foreign tax obligations on top of U.S. ones. The administrative complexity is significant, and the tax benefits depend heavily on the destination country's tax treaty with the United States and the specific income types involved. A formal pre-departure tax review with a cross-border tax specialist is the appropriate starting point.

Final Thoughts

For high earners weighing a move, plan for the tax implications even if they're not the primary reason for moving. Model state taxes against your income profile, review California or other state-specific clawback rules, and research the effects of moving relative to an anticipated liquidity event.

The tax math on a move is the part you can model yourself. Working through the rest of the decision is easier with peers who have done it.

Long Angle's Trusted Circles are small, confidential peer advisory groups of 6 to 8 members matched by life stage and wealth complexity, meeting monthly with a facilitator who is also a financial professional. For members weighing a relocation alongside a business sale, equity event, or next-chapter transition, Trusted Circles are designed for exactly this kind of decision.

More From Long Angle

Beyond Wealth Newsletter

Long Angle's free weekly newsletter covering wealth management, investing and life at the intersection of money and ambition. Subscribe »

Navigating Wealth Podcast

The Long Angle podcast. Founders and executives on the financial and personal decisions that actually matter. Listen »